Is crypto halal? That's not a question with a clean yes or no answer - and any article that claims otherwise is glossing over a genuine, unresolved debate between some of the most respected Islamic scholars alive today. Whether you're a practicing Muslim who wants to participate in DeFi, someone exploring Bitcoin as an alternative store of value, or a trader trying to reconcile your faith with your portfolio, the permissibility question ultimately depends on what you're buying, how you're trading it, and why you're doing it.

This guide cuts through the noise. I've structured it around the three Islamic finance principles that actually matter - Riba, Gharar, and Maisir - and mapped real scholarly positions to each. No single fatwa covers every cryptocurrency. The analysis below will give you the framework to evaluate each asset and activity on its own terms.

⚡ Key Takeaways

- No single fatwa covers all cryptocurrencies - assessment depends on the specific asset and how it's used

- Riba-free structure is crypto's strongest argument for halal status; leverage and lending products reintroduce Riba risk

- Scholars are genuinely split - both the halal and haram positions are grounded in legitimate Islamic legal reasoning

- Meme coins, privacy coins, and leveraged derivatives are the categories most consistently flagged as impermissible

- Consulting a qualified Islamic finance scholar remains the recommended path for significant investment decisions

What Is Cryptocurrency? Foundations Every Muslim Investor Must Know

Cryptocurrency is a decentralised digital asset secured by cryptography and recorded on a distributed ledger called a blockchain. No single government, central bank, or institution controls it. Transactions are verified by a global network of participants rather than a trusted intermediary - and that structural fact sits at the centre of the halal debate.

Bitcoin was the first and remains the most widely discussed cryptocurrency in Islamic rulings. Ethereum followed, introducing programmable smart contracts that now power a vast ecosystem of decentralised finance applications. Today there are thousands of cryptocurrencies, but most scholarly analysis still centres on Bitcoin and Ethereum because they have the longest track record and the most fatawa issued against them.

Before applying Islamic law to crypto, one foundational question must be answered: does cryptocurrency qualify as Mal - the Islamic legal concept of valid, ownable property? For an asset to be treated as property under Shariah, it must be capable of ownership, capable of storage, and possess commercial value (Mutaqawwam). Widely accepted digital assets satisfy all three conditions: they can be owned via a wallet, stored securely, and traded at market-recognised value.

Blockchain, Decentralisation, and the Concept of Mal in Islamic Law

Blockchain's transparency is one of its strongest arguments for Islamic permissibility. Every transaction is permanently recorded on a public ledger - traceable, auditable, and resistant to falsification. That aligns directly with Islamic finance's emphasis on accountability and the prevention of fraud.

Crucially, peer-to-peer crypto transfers don't inherently charge or pay interest. No built-in Riba mechanism exists in the base protocol - which is a meaningful distinction from conventional banking. That said, products built on top of crypto protocols - lending platforms, yield-bearing savings accounts, leverage products - can and often do reintroduce Riba. The protocol and its application layer are separate questions.

Is Crypto Halal or Haram? What Scholars Actually Say

If you've searched this question and found contradictory answers, that's not because the sources are unreliable. Genuinely qualified Islamic scholars, working from the same foundational texts, have arrived at opposite conclusions. The disagreement is real, and it reflects the genuine complexity of applying centuries-old legal frameworks to an asset class that didn't exist until 2009.

Scholarly Arguments That Cryptocurrency Is Halal

Three scholarly voices have been most influential in the halal camp:

- Mufti Muhammad Abu-Bakar (former Shariah advisor, Blossom Finance) - His 2017 working paper remains one of the most cited analyses in the field. Abu-Bakar concluded that Bitcoin functions as a permissible medium of exchange: it is accepted as payment by merchants, priced by markets, and capable of being owned and transferred. His argument that all currencies carry a speculative element - and that this alone doesn't render them haram - directly addressed critics who pointed to Bitcoin's volatility.

- Mufti Faraz Adam - A prominent UK-based Islamic finance scholar, Adam has publicly supported Bitcoin's permissibility when used as a financial instrument rather than a speculative vehicle. His position emphasises that the asset's nature matters more than its market behavior.

- Ziyaad Mahomed (Shariah Committee Chairman, HSBC Amanah Malaysia Bhd) - Mahomed argues that Shariah doesn't require a currency to have intrinsic physical value. Social acceptance establishes monetary value, and Bitcoin - used in transactions across dozens of countries - passes that test. He does add a meaningful caveat: when retail-driven speculation pushes prices into irrationally inflated territory, the activity starts to look more questionable.

The common thread across all three positions: absence of Riba in the base protocol, blockchain's transparency aligning with Islamic ethics, and fulfilment of the Mal property requirement.

Scholarly Arguments That Cryptocurrency Is Haram

The haram position is equally well-grounded in Islamic legal principles:

- Grand Mufti of Egypt, Shaykh Shawki Allam - Egypt's highest religious authority ruled that Bitcoin is impermissible, citing excessive uncertainty in pricing, the absence of any sovereign or institutional backing, and the cryptocurrency's documented use by criminal actors. He also flagged the technical barrier to entry - securing a private key requires a level of sophistication far beyond ordinary currency use - as evidence that Bitcoin functions differently from recognised financial instruments.

- Shaykh Haitham al-Haddad - His Arabic-language analysis argues that Bitcoin lacks the foundational value basis required of a legitimate currency. Unlike fiat currencies, which at minimum carry state authority, no authority backs Bitcoin. He goes further: by extension, Bitcoin mining - the process of creating new coins through computational work - is impermissible because it generates money from nothing.

- Turkish Religious Authority (Diyanet İşleri Başkanlığı) - Turkey's state religious authority issued a ruling against Bitcoin on grounds of excessive uncertainty (Gharar) and potential for abuse by criminal elements. This carries institutional weight as an official state-level Islamic legal position.

Halal vs. Haram Cryptocurrencies - Comparison Table

No asset gets a universal ruling, but scholars' assessments of specific cryptocurrencies follow a recognisable pattern. Always ensure you understand how to store and access crypto assets safely before making any investment decision.

This table reflects general scholarly discussion, not a universal fatwa. Individual scholars and specific use cases can alter any assessment. Consult a qualified Islamic finance scholar before making investment decisions.

The Three Core Islamic Finance Principles Applied to Crypto

Every Shariah assessment of cryptocurrency ultimately comes back to three foundational prohibitions. Understanding them isn't academic - it's the practical toolkit every Muslim investor needs.

Three practical examples to make this concrete:

Riba example: Celsius Network - before its collapse - paid fixed interest on deposited crypto. That product structure, where you deposit an asset and receive a predetermined return regardless of market performance, mirrors conventional interest-bearing accounts. Most Islamic scholars who reviewed it classified it as impermissible for exactly this reason.

Gharar example: A perpetual futures contract with no defined expiry and liquidation mechanics tied to funding rates creates layered uncertainty - uncertain price, uncertain funding cost, uncertain liquidation threshold. That stacking of ambiguity sits firmly in Gharar territory.

Maisir example: Buying a meme coin because a social media influencer said it would "pump" represents a transaction with no productive economic basis. The buyer has no claim to any underlying business, asset, or utility. That pattern is what Islamic scholars mean when they invoke Maisir - it functions like a bet, not an investment.

How to Evaluate Whether a Cryptocurrency Is Shariah-Compliant

Rather than waiting for a comprehensive fatwa on every crypto token, Muslim investors can apply a structured screening process. This checklist is a starting point - not a substitute for a scholar's personal opinion on significant investment decisions.

6-Step Shariah Compliance Checklist:

- Mal Test - Can this asset be owned, stored, and traded at a recognised market value? If yes, it passes the fundamental property test. If it's a token with no market depth, no practical use, and no mechanism for establishing value, it fails.

- Riba Test - Does holding, using, or trading this asset require paying or receiving interest? Check whether the platform charges swap fees (common on leveraged positions), whether the token accrues yield through lending, or whether the staking mechanism resembles an interest payment rather than genuine profit-and-loss sharing.

- Legitimate Purpose Test - What economic function does this asset serve? Bitcoin: medium of exchange and store of value. Ethereum: powers a computing platform. Dogecoin: social meme. The strength of the use case correlates directly with its Islamic permissibility argument.

- Gharar Assessment - How volatile is this asset, and does that volatility represent genuine market uncertainty (acceptable) or speculative frenzy without fundamentals (impermissible)? Consider whether the asset's price is connected to any underlying economic activity.

- Transparency Test - Are transactions traceable? Is the project's code open-source? Can you verify who controls the asset and how it's issued? Privacy coins that deliberately obscure these answers fail this test.

- Prohibited Industry Check - Is the token connected to gambling, alcohol, pornography, predatory lending, or any other haram industry? Many token ecosystems are straightforwardly disqualifying on this basis alone.

📊 Practical Guidance

If a cryptocurrency passes steps 1-3 and doesn't dramatically fail steps 4-6, it likely falls within the range that halal-camp scholars would consider permissible for spot trading. If it fails multiple tests, seek a scholar's opinion before proceeding with significant capital.

Centralised Exchange vs. Decentralised Exchange vs. Shariah-Certified Platform

Where you trade can be as important as what you trade. Three platform models dominate the market, each with different implications for Shariah compliance:

CEX platforms aren't categorically haram, but they frequently bundle products - flexible savings, crypto loans, leveraged instruments - that require individual screening. Using a CEX for spot trading while deliberately avoiding its lending and margin products is a defensible approach. DEX platforms, by contrast, are structurally closer to Islamic finance values: no intermediary, no interest-charging institution, user-controlled custody.

Red Flags - What Makes a Cryptocurrency Haram

Pattern recognition matters here. These are the warning signs that should prompt immediate caution or a full stop:

⚠ Haram Red Flags by Shariah Principle

- Riba Red Flags: Fixed-yield crypto savings accounts; crypto lending platforms paying set APY; swap fees on leveraged positions that resemble interest; yield tokens distributing lending revenue

- Gharar Red Flags: Perpetual futures with undefined settlement; margin trading with funding-rate liquidation; tokens with no clear ownership structure; projects whose value depends entirely on future promises

- Maisir Red Flags: Meme coins with no utility driven purely by social virality; pump-and-dump schemes; casino and gambling-linked tokens; day-trading behavior with no connection to the asset's economic purpose

If a crypto product promises fixed returns without risk, treat it as Riba until a qualified scholar confirms otherwise. That single heuristic will filter out the majority of impermissible products in the market today.

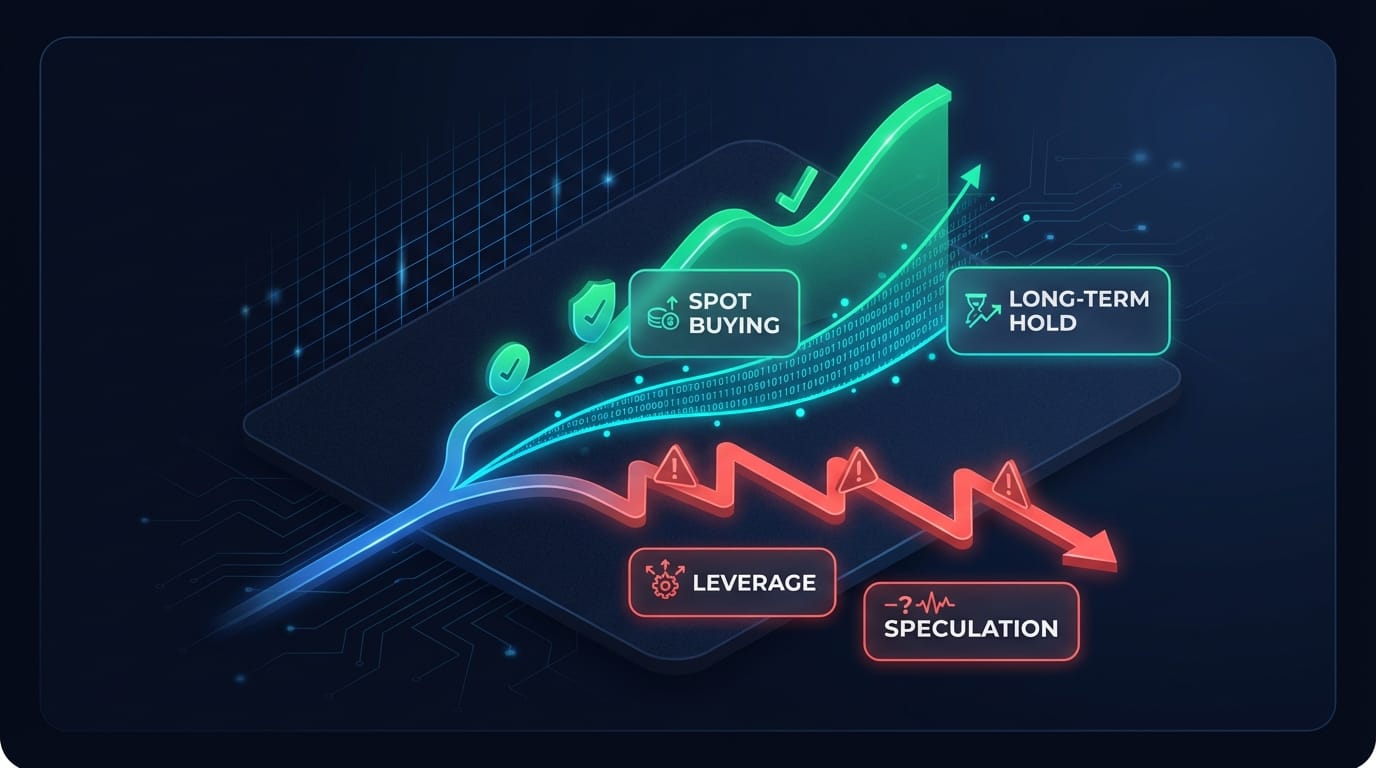

Halal Crypto Investment: Permissible Strategies for Muslim Investors

Not all crypto activity is off the table. The question isn't only whether crypto is permissible - it's how a Muslim investor can structure their engagement to stay within Shariah guidelines. Purpose and transaction structure determine compliance more than the asset class itself.

A brief note on Zakat: Muslim investors who hold cryptocurrency above the nisab threshold (the minimum wealth level that triggers Zakat obligation) are required to include that holding in their Zakat calculation. The nisab is typically calculated against the equivalent value in gold or silver. If you hold Bitcoin or Ethereum that exceeds this threshold for a full lunar year, 2.5% is due. This is an area where most published guides fall short - Zakat on crypto is a practical obligation for any Muslim with meaningful holdings.

Permissible Crypto Strategies - Spot Buying, HODL, and Long-Term Investing

Spot buying with immediate settlement and full ownership transfer passes the Islamic finance test most cleanly. The buyer pays, ownership transfers, and no interest obligation exists. Long-term holding of a fundamentally sound asset - particularly Bitcoin or Ethereum - resembles Shariah-compliant equity investment far more than it resembles gambling. HODL isn't just a crypto meme; structurally, it's the most defensible approach under Islamic finance principles.

Day trading sits in a grey zone. Some scholars allow carefully structured short-term trades when ownership is genuine and speculation is restrained. Others - citing Maisir - prohibit it categorically. Leverage and margin trading deserve a clear assessment: the mechanics introduce Riba through funding rates, amplify Gharar through liquidation risk, and the activity pattern often constitutes Maisir. Crypto trading involves substantial risk of loss in any form - in leveraged positions, that risk is magnified significantly.

Shariah-Compliant Alternatives to Cryptocurrency

For Muslim investors who conclude that crypto's current risk profile - or the absence of scholarly consensus - makes meaningful exposure difficult to justify, the Islamic finance ecosystem offers credible alternatives:

- Sukuk (Islamic Bonds) - Fixed-income instruments structured without interest. Returns come from underlying asset performance or revenue-sharing, not interest. Available through Islamic banks and dedicated investment platforms.

- Shariah-screened equity funds and halal ETFs - Diversified exposure to companies that pass Islamic finance screening criteria (no prohibited industries, manageable debt levels, screened revenue sources).

- Gold - Classically halal as a store of value. Spot gold purchases meet the Mal and no-Riba criteria cleanly. Gold-backed crypto tokens like OneGram bridge the traditional halal asset with blockchain technology, offering a hybrid option for investors comfortable with digital assets.

- Islamic crowdfunding (Shariah-compliant SME finance) - Profit-and-loss sharing structures that invest directly in businesses rather than speculating on assets. Platforms operating under this model provide genuine economic participation - the core of what Islamic finance considers permissible investment.

These alternatives aren't consolation prizes. They're established, regulated, and growing - and for investors who want exposure to genuine economic activity without crypto's current regulatory and volatility uncertainty, they represent a coherent portfolio strategy.

Conclusion - Is Crypto Halal? A Balanced Verdict for Muslim Investors

Is crypto halal? The accurate answer is: it depends - and that dependence is on factors you can evaluate systematically.

For conservative investors: The scholarly debate remains open, and the volatility concerns raised by haram-position scholars are grounded in legitimate Islamic legal reasoning. Until Islamic finance bodies issue clearer, more comprehensive guidance - and until crypto's regulatory environment stabilises - Sukuk, halal ETFs, and gold remain lower-ambiguity options for wealth preservation and growth.

For moderate investors: Spot buying of well-established, transparent cryptocurrencies - primarily Bitcoin and Ethereum - with no leverage, after seeking personal scholarly guidance, falls within the range that respected halal-position scholars have found defensible. The Mal test is satisfied. Riba is absent from the base transaction. The transparency of blockchain ledgers aligns with Islamic finance values. Keep Zakat obligations in mind for holdings above the nisab.

For active traders: Leverage, perpetual futures, and margin products introduce Riba and Gharar that put them outside what most scholars consider permissible. Day trading's Maisir exposure is real and contested. Until the field develops more specific guidance on algorithmic and systematic trading within Islamic finance, caution is the rational default.

The trajectory of this debate matters. As crypto infrastructure matures, as Shariah-certified platforms multiply, and as more Islamic finance institutions develop crypto-specific governance frameworks, the question of is crypto halal will become progressively easier to answer with specificity. The on-chain verifiability that blockchain enables - every transaction traceable, every rule codified in open-source code - aligns meaningfully with the transparency principles at the heart of Islamic finance.

Consult a qualified Islamic finance scholar before making significant investment decisions. This article provides an educational framework - the final ruling on your specific situation belongs with a qualified jurist.

Crypto trading involves substantial risk of loss. This article is educational in nature and does not constitute financial or religious advice. Always seek guidance from a qualified Islamic finance scholar for personal investment rulings.

Last updated: March 2026.

Frequently Asked Questions

Is crypto halal or haram in Islam?

There is no single, universally accepted ruling. Scholarly opinion divides into two credible camps: those who permit cryptocurrency as a legitimate medium of exchange and digital asset (Mufti Abu-Bakar, Mufti Faraz Adam, Ziyaad Mahomed), and those who prohibit it on grounds of excessive uncertainty (Gharar), speculation resembling gambling (Maisir), and lack of intrinsic value (Grand Mufti of Egypt, Shaykh Haitham al-Haddad). The verdict depends on which cryptocurrency, which platform, and how you're using it. For significant investment decisions, seek a personal fatwa from a qualified Islamic finance scholar familiar with the current state of the crypto market.

Is Bitcoin halal according to Islamic scholars?

Bitcoin has attracted the most scholarly attention of any cryptocurrency. The halal position holds that Bitcoin qualifies as valid property (Mal), functions as a medium of exchange accepted by merchants globally, and involves no built-in Riba in its base transactions. Mufti Abu-Bakar's 2017 analysis and subsequent endorsements support this view. The haram position, represented by Egypt's Grand Mufti and Shaykh Haitham al-Haddad, argues that Bitcoin lacks intrinsic value, is excessively volatile, and carries no institutional backing. Both positions are grounded in legitimate Islamic jurisprudence - the debate reflects genuine legal complexity, not one side simply being uninformed.

Which cryptocurrencies are generally considered halal?

Bitcoin and Ethereum are most commonly discussed as permissible by halal-position scholars - Bitcoin for its role as a medium of exchange, Ethereum for powering smart contracts with genuine economic utility. Shariah-certified tokens like OneGram (gold-backed) and X8 Currency (real-asset backed) are designed explicitly for Islamic finance compliance. The common thread: genuine utility, traceable transactions, no prohibited industry connections, and an established market that satisfies the Mal (property) requirement under Islamic law.

Is crypto day trading halal or haram?

Opinion is divided. Many scholars consider high-frequency speculation equivalent to Maisir - particularly when the trader has no interest in the asset's underlying purpose and is purely betting on short-term price movement. Others distinguish between genuine short-term analysis-based trading and pure speculation, allowing the former in limited cases. The practical guidance: ensure each trade involves genuine ownership transfer, avoid any margin or leverage, and honestly assess whether your trading pattern resembles investment or a bet. Consult a qualified scholar if the answer is unclear.

Is leverage or margin trading crypto haram in Islam?

By the standards of most Islamic scholars who have reviewed the question, leveraged and margin trading is generally considered impermissible. Margin positions require borrowing capital - a lending arrangement that typically incurs interest-like funding costs, introducing Riba. The forced liquidation mechanics create extreme Gharar, since your position can be automatically closed at a point you don't control. The activity pattern of using borrowed money to amplify speculative positions concentrates the very behaviors that Islamic finance was designed to prevent. Crypto trading with leverage also involves substantial risk of loss that can exceed your initial capital.

How do I know if a cryptocurrency is Shariah-compliant?

Apply six checks: (1) Mal test - can it be owned and stored with recognised commercial value? (2) Riba test - does using it require paying or receiving interest? (3) Legitimate purpose test - what real economic function does it serve? (4) Gharar assessment - is the uncertainty level within acceptable limits? (5) Transparency test - are transactions traceable and the project's mechanics auditable? (6) Prohibited industry check - does the token connect to gambling, alcohol, or other haram sectors? An asset that passes the first three and doesn't dramatically fail the remaining three is defensible under most halal scholarly positions.

Do I need to pay Zakat on my cryptocurrency holdings?

Yes, if your crypto holdings exceed the nisab threshold and have been held for a full lunar year (hawl). The nisab is typically calculated as the equivalent of 85 grams of gold or 595 grams of silver in current market value. Cryptocurrency is treated as a tradeable asset under most scholarly opinions, making it subject to the standard 2.5% Zakat rate. Calculate your total crypto holdings at market value, subtract any liabilities, and if the net amount exceeds nisab after a full lunar year, 2.5% is due. Consult a qualified Islamic finance scholar or a dedicated Zakat calculation service for holdings across multiple platforms or staking arrangements.