Mirror Protocol was one of DeFi's most ambitious experiments: a protocol that let anyone, anywhere, trade synthetic versions of stocks, ETFs, and other real-world assets - directly on-chain, without a broker, without a bank account, and without borders. Built on the Terra blockchain by Terraform Labs, it minted tokenized "mirrored" assets (mAssets) that tracked real-world prices and could be traded 24/7 on decentralized exchanges.

The protocol shut down in 2022 following the collapse of the Terra ecosystem. But understanding how Mirror Protocol worked - its collateral mechanics, synthetic asset design, and governance model - remains essential knowledge for anyone serious about DeFi.

⚡ Key Takeaways

- Mirror Protocol was a DeFi protocol on the Terra blockchain that enabled synthetic assets (mAssets) tracking real-world stocks, ETFs, and crypto

- mAssets are blockchain tokens that mirror the price of underlying assets without requiring ownership of those assets

- The MIR token served as Mirror's governance and reward distribution mechanism

- Collateralized Debt Positions (CDPs) with a minimum 150% collateral ratio backed all mAsset creation

- Mirror Protocol ceased operations in December 2022 following the Terra/UST collapse in May 2022

What Is Mirror Protocol? Definition and Core Concept

Mirror Protocol was a decentralized finance (DeFi) protocol built on Terra's blockchain using CosmWasm smart contracts. Its core function: allow users to issue and trade synthetic assets - called mAssets - that tracked the price of real-world financial instruments without requiring anyone to actually own the underlying asset.

The value proposition was genuinely radical at the time. A trader in a region without access to US equity markets could gain price exposure to Tesla, Apple, or an S&P 500 ETF by minting a synthetic token - no brokerage account, no KYC, no geographic restriction. The protocol ran permissionlessly, with no central authority controlling access or outcomes. All positions and collateral were verifiable on-chain.

Terraform Labs launched Mirror in December 2020. By mid-2021, it had grown into one of the top 15 DeFi protocols by total value locked (TVL), with over $118 million in collateral secured on the platform. That growth reflected genuine demand for decentralized access to traditional financial markets - a gap that DeFi had struggled to address before Mirror.

mAssets are composable and portable. They weren't confined to the Terra blockchain - they were also accessible on Ethereum and Binance Smart Chain via cross-chain bridges, making them one of the more interoperable synthetic asset products in the early DeFi era.

What Are mAssets (Mirrored Assets)?

mAssets are blockchain tokens that track the price of real-world assets without requiring ownership of the underlying. Each token carries a small "m" prefix followed by the underlying asset's ticker: mTSLA for Tesla, mMSFT for Microsoft, mAAPL for Apple, mQQQ for the Invesco QQQ ETF, mBTC for Bitcoin, mETH for Ether, mGME for GameStop.

Price accuracy came from Band Protocol oracle feeds, which updated every 30 seconds. That oracle price governed all collateral requirements and served as the benchmark against which AMM pool prices were compared.

A few properties made mAssets distinctly different from traditional stock access. They traded 24/7 - unlike the NYSE or Nasdaq, which operate on fixed market hours. They supported fractional ownership natively: a user could hold $10 worth of a $500 stock without any platform-specific fractional share infrastructure. And they could only be minted during real-world market hours (to ensure fresh oracle data), but once minted, they traded continuously.

How Does the Collateralization Mechanism Work?

Every mAsset in existence was backed by a Collateralized Debt Position (CDP). To mint a mAsset, a user deposited collateral into the protocol - at a minimum, 150% of the current value of the real-world asset being synthesized. This minimum collateralization ratio (MCR) was the protocol's primary safety mechanism.

Accepted collateral: TerraUSD (UST) stablecoins, or other mAssets already in the system.

Here's the practical flow with a concrete example:

The 1.5% CDP closure fee didn't go to the protocol treasury - it went to MIR token stakers, creating a direct revenue-sharing mechanism between protocol activity and token holders.

Liquidation risk was real and meaningful. A user who opened a CDP at exactly 150% MCR had zero buffer - any upward price movement in the underlying asset would trigger liquidation. Experienced users typically over-collateralized to 200-250% to maintain a safety margin, accepting the capital inefficiency in exchange for position security.

Who Created Mirror Protocol?

Mirror Protocol was conceived in early 2020 and launched in December 2020 by Terraform Labs (TFL), the South Korean blockchain company behind the Terra network. The project was co-founded by Do Kwon, who served as CEO of Terra, and Daniel Shin, who had previously founded TicketMonster (a major Korean e-commerce platform) and later Chai, a Seoul-based payments startup. Kwon himself had stints at both Microsoft and Apple before pivoting to crypto.

One of the more notable design choices TFL made from day one: no premine, no owner keys, no token allocation to the team. The entire MIR supply was distributed to the community through staking rewards and airdrops. Governance rights and economic upside were intentionally placed entirely in the hands of users - a genuine commitment to decentralization that was less common among 2020-era DeFi protocols.

That decentralization, unfortunately, also meant Mirror Protocol had no controlling party capable of stabilizing or restructuring operations when the ecosystem it depended on collapsed.

In May 2022, TerraUSD (UST) - the stablecoin underpinning all mAsset collateral - lost its dollar peg catastrophically. The death spiral that followed wiped out the Terra ecosystem within days. Mirror Protocol, entirely dependent on UST as its collateral base, became effectively insolvent. The protocol ceased all operations in December 2022.

Despite its shutdown, Mirror Protocol's architecture remains a foundational case study in synthetic asset design - what worked, what the failure modes were, and how successor protocols have iterated on the model.

How Does Mirror Protocol Work? The Four Core Functions

Mirror Protocol's design centered on four interdependent functions: minting, trading, liquidity providing, and staking. Each fed into the others - minted assets created trading supply, trading generated fees that powered liquidity rewards, and staking MIR governed the whole system. Understanding how these functions interlocked is key to understanding both the protocol's strength and its structural vulnerabilities.

The underlying infrastructure for all trading was Terraswap - an automated market maker (AMM) built on Terra - with mAssets listed against UST.

Minting mAssets

Minting was the entry point into the Mirror ecosystem. A user opened a CDP, posted collateral above the 150% MCR, and received freshly minted mAsset tokens in return. Those tokens could then be held as price exposure, traded on Terraswap, staked into liquidity pools, or used as collateral for additional CDPs.

Minters weren't just passive position-takers. The protocol recognized two distinct roles: minters, who created synthetic assets and took on collateral management responsibilities; and shorters, who minted mAssets specifically to sell them immediately - capturing any price premium between the AMM pool price and oracle price. The full mechanics of the shorting mechanism are covered in the pricing section below.

Trading mAssets

Once minted, mAssets traded on Terraswap using an x.y=k constant product AMM - the same model as Uniswap. All pairs were listed against UST, Mirror's trading base currency. The protocol also enabled mAsset trading on Ethereum (via Uniswap) and Binance Smart Chain through cross-chain bridges.

📊 Fee Summary - Mirror Protocol Trading Costs

- Terraswap trading fee: 0.30% per trade

- CDP closure fee: 1.5% of collateral (charged on CDP close)

- Break-even on long position: minimum 0.6% price move

- Break-even on short position: minimum 2.1% price move

The 24/7 trading availability was a genuine differentiator. Traditional equity markets close on weekends and holidays - mAssets didn't. That feature was particularly relevant for assets like mGME during high-volatility events that often developed outside US market hours.

Providing Liquidity and Staking

Liquidity providers on Mirror deposited equal values of a mAsset and UST into Terraswap pools. In return, they received LP (Liquidity Provider) tokens representing their share of the pool. Those LP tokens accumulated rewards from pool trading fees - and could then be staked on Mirror Protocol itself to earn additional MIR token rewards.

LIQUIDITY PROVISION FLOW

Step 1

Deposit mAsset + UST (equal value) into Terraswap pool

Step 2

Receive LP tokens representing your pool share

Step 3 - Key action

Stake LP tokens on Mirror Protocol → earn MIR rewards continuously

Step 4

Unstake anytime - no lockup requirement

Step 5

Burn LP tokens → reclaim mAsset + UST from pool

Staking MIR directly in the governance smart contract offered a different reward stream: governance stakers received a share of the CDP closure fees (via the MIR buyback mechanism) and earned the right to vote on protocol proposals.

For advanced users, Mirror v2 introduced a delta-neutral yield strategy - holding simultaneous long and short positions of equal size to eliminate directional price exposure while earning yield from both the long LP farm and the short LP (sLP) farm. The strategy required careful calibration (collateral requirements vary by mAsset), but on assets with 200% collateral requirements, the mechanics were relatively clean: split the position evenly between long and short, deposit equal UST on the long side, and post 3.5x the position size as collateral on the short.

One honest caveat: liquidity providers faced impermanent loss risk. On a 50% price move in the underlying mAsset, IL from the LP pool historically ran around 4%. That's not catastrophic for longer-term positions with strong farm yields - but it's a real drag that needs to be modeled into any liquidity provision strategy.

The MIR Token - Utility, Tokenomics, and Value

MIR served two primary functions in the Mirror ecosystem: governance and reward distribution. But the tokenomics design had an elegant mechanic that created genuine demand pressure on MIR beyond speculative interest.

Governance: MIR holders staked their tokens to vote on protocol proposals - whitelisting new mAssets, adjusting MCRs, changing trading fees, and allocating community pool funds. Passing a governance proposal required a majority of staked MIR and typically took one week to take effect.

Revenue sharing: Every CDP closure generated a 1.5% fee on the collateral. That fee was used to buy MIR tokens on Terraswap, which were then distributed to MIR stakers. Protocol activity → buyback → staker reward. This created a direct link between platform usage and token holder returns - without relying on token inflation to fund rewards.

Total planned supply: approximately 370-375 million MIR, issued over four years. Inflation was front-loaded and designed to decrease over the issuance period - targeting roughly 15% annual inflation by year four. The finite supply and decreasing issuance schedule were positioned as an anti-inflation mechanism that would make MIR increasingly scarce relative to protocol demand.

That value thesis collapsed entirely with the Terra ecosystem in May 2022. Post-shutdown, MIR's utility became moot - but the tokenomics model itself (no team allocation, fee-funded buybacks, governance-tied staking) remains influential in how subsequent DeFi protocols have approached token design.

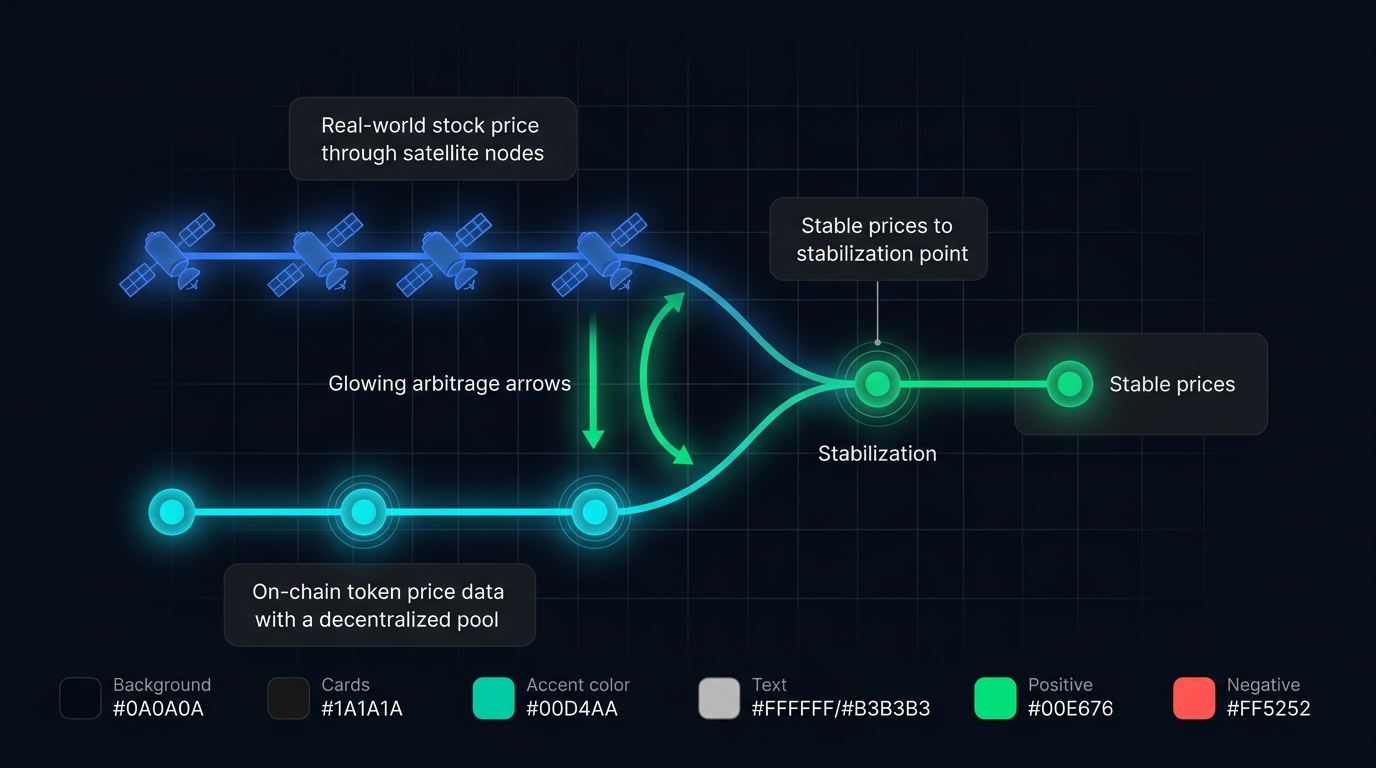

The mAsset Pricing Mechanism - Oracles, Arbitrage, and Peg Stability

This is where Mirror Protocol's design gets genuinely sophisticated - and where most surface-level explanations fall short.

Three interlocking mechanisms maintained the soft peg between mAsset prices on Terraswap and the real-world prices of underlying assets:

1. Oracle price feeds

Band Protocol provided real-world asset price data every 30 seconds. This "oracle price" governed all CDP collateral requirements and served as the reference for arbitrage activity. The oracle price and the AMM pool price weren't always identical - that gap is where the system's self-correcting dynamics kicked in.

2. Minting liquidations

When the price of a real-world asset rose and a CDP's collateral fell below the 150% MCR, the protocol automatically sold collateral to buy back the mAsset. That buying pressure drove the mAsset's pool price upward - toward the oracle price - while simultaneously restoring the collateral ratio. The mechanism was automatic, on-chain, and required no human intervention.

3. Arbitrage

When mAsset pool price diverged from oracle price, arbitrageurs stepped in. Here's how the math worked in practice:

Mirror v2 introduced short LP (sLP) tokens specifically to address persistent price premiums. When a user minted an mAsset and sold it immediately to capture a premium, they received sLP tokens instead of standard LP tokens. Staking those sLP tokens generated additional MIR rewards - creating a financial incentive to mint and sell specifically when premiums were elevated. The mechanism kept premiums within a narrow band and improved price tracking accuracy significantly vs. v1.

The 30-second oracle update frequency was a deliberate design choice. More frequent updates increase accuracy but create more opportunities for price manipulation; less frequent updates leave larger windows for premium exploitation. Band Protocol's 30-second cadence represented a reasonable operational tradeoff for the asset types Mirror supported.

Risks, Limitations, and the Terra Collapse

Mirror Protocol's technical design was sophisticated. Its fatal flaw was structural: every mAsset in the system was collateralized by TerraUSD (UST), an algorithmic stablecoin whose peg depended entirely on demand for LUNA - Terra's native token.

When UST began losing its peg in May 2022, the death spiral was fast and brutal. LUNA's price collapsed trying to absorb UST redemptions. That collapse destroyed the value of UST. That destruction made all mAsset CDPs effectively insolvent. Mirror Protocol ceased operations in December 2022.

Four risk categories defined the Mirror experience:

⚠ Risk Summary - Mirror Protocol

- Systemic / Counterparty Risk → Mirror's entire collateral base was UST. A failure of UST was a single point of failure for the entire protocol. When it failed, there was no fallback.

- Liquidation Risk → CDPs opened near the 150% MCR could be liquidated by any upward price movement in the underlying asset. Users who under-collateralized paid for efficiency with forced liquidations.

- Impermanent Loss → Liquidity providers faced IL whenever mAsset prices moved significantly vs. UST. On a 50% price move, historical IL ran approximately 4% of position value.

- Smart Contract Risk → All DeFi protocols carry code vulnerability risk. Mirror was audited, and TFL maintained open bug bounties - but no audit eliminates risk entirely.

The Terra collapse is not a footnote in Mirror Protocol's story. It is the story's defining chapter - and a case study every serious DeFi participant should understand. The lesson isn't that synthetic assets are unviable. It's that collateral quality is the load-bearing wall of any CDP-based system. UST's algorithmic peg was the weakness that brought the entire structure down.

Crypto trading and DeFi participation involves substantial risk of loss. Protocol failures, smart contract exploits, and market volatility can result in partial or total loss of funds. Nothing in this article constitutes financial advice.

Mirror Protocol's Legacy and Alternatives in Synthetic Asset DeFi

Mirror Protocol didn't survive - but its influence on synthetic asset design is visible in nearly every protocol that followed. The CDP model, oracle-based price feeds, community governance with no team allocation, and the delta-neutral yield farming concept all became reference points for the next generation of on-chain derivatives infrastructure.

For users who want similar functionality today, several protocols carry the synthetic asset concept forward - each with different tradeoffs:

The Synthetix model is probably Mirror's closest living descendant in terms of intent - permissionless, on-chain synthetic exposure to real-world assets. But Synthetix uses a shared debt pool rather than individual CDPs, which eliminates per-user liquidation risk at the cost of system-wide exposure to the overall collateral ratio.

dYdX takes a different approach entirely: perpetual futures contracts rather than synthetic ownership tokens. Users get price exposure through leverage rather than minting - no CDP, no collateral management, just long or short positions. For traders who want directional exposure without the complexity of CDP management, perpetuals infrastructure has largely displaced the Mirror model.

For passive exposure to real-world assets, protocols like Ondo Finance and Backed Finance offer tokenized versions of US Treasuries and equities that are directly backed by the underlying assets - a structurally safer approach than algorithmic synthetics, though with different access requirements and regulatory considerations.

Platforms built on self-custody and on-chain verifiability - where users control their own funds and all outcomes are transparently verifiable - represent the trajectory that DeFi is moving toward. Zipmex reflects this direction: self-custodial, on-chain, with real yield generated from platform activity rather than token emissions.

Conclusion - Mirror Protocol's Place in DeFi History

Mirror Protocol's story doesn't fit neatly into a hero or villain narrative. It was a technically sophisticated, genuinely innovative protocol that proved something important: permissionless, borderless access to real-world asset prices is achievable on-chain. The CDP model worked. The oracle integration worked. The governance design worked. What failed wasn't Mirror Protocol's architecture - it was the collateral layer beneath it.

For the DeFi researcher: Mirror Protocol set architectural precedents that remain relevant. Its oracle-AMM-arbitrage pricing mechanism, the delta-neutral sLP yield strategy, and its no-premine governance model were ahead of their time. Study the protocol not as a failure story but as a design document.

For the active DeFi practitioner: The collapse of Mirror reinforces a principle that holds across every CDP-based protocol: collateral quality is everything. UST was algorithmically pegged with no hard asset backing - a fragile foundation for a synthetic asset ecosystem. When evaluating similar protocols today, the first question should always be: what is the collateral, and what happens if it fails?

For the risk-aware investor: Mirror Protocol is a landmark case study in systemic DeFi risk. A technically sound protocol with over $1 billion in TVL at its peak was rendered worthless in days - not by a hack, not by a governance failure, but by a single-point-of-failure in its collateral design. Diversification, collateral quality, and protocol interdependency assessment are not optional analysis for anyone deploying capital in DeFi.

Mirror Protocol ceased operations in 2022. Its innovations in synthetic asset design, however, continue to shape what gets built next. Real-world asset tokenization on-chain is not a solved problem - it's an active frontier. The protocols solving it today are iterating on exactly the foundations Mirror laid down. For a deeper look at how the broader DeFi ecosystem has evolved since, the fundamentals established here remain relevant starting points.

Last updated: April 2026.

Frequently Asked Questions

What is Mirror Protocol in simple terms?

Mirror Protocol was a DeFi protocol built on the Terra blockchain that allowed anyone to create and trade synthetic versions of real-world assets - stocks, ETFs, and cryptocurrencies - without owning the underlying assets. These synthetic tokens, called mAssets, tracked real prices through oracle feeds and could be traded 24/7 on decentralized exchanges. The protocol launched in December 2020 and shut down in December 2022 following the collapse of the Terra ecosystem and its UST stablecoin.

What are mAssets (Mirrored Assets)?

mAssets are blockchain tokens that mirror the price of real-world financial assets without requiring ownership of those assets. Each mAsset carries a small "m" prefix: mTSLA tracks Tesla stock, mQQQ tracks the Invesco QQQ ETF, mBTC mirrors Bitcoin. They're created through collateralized minting, trade 24/7 on AMMs like Terraswap, and can represent stocks, ETFs, or other cryptocurrencies. Price accuracy is maintained through Band Protocol oracle feeds updating every 30 seconds, combined with arbitrage mechanisms that close any gap between the oracle price and trading price.

How does Mirror Protocol create synthetic assets?

Mirror Protocol creates synthetic assets through Collateralized Debt Positions (CDPs). A user deposits collateral - primarily TerraUSD (UST) - worth at least 150% of the target mAsset's current value, creating a CDP. The protocol then mints the corresponding mAsset tokens, which the user receives. This over-collateralization ensures the system remains solvent even if asset prices rise. If the collateral ratio falls below the 150% minimum, the protocol automatically liquidates the position to restore solvency.

Is Mirror Protocol still active in 2026?

No. Mirror Protocol is no longer operational. The protocol ceased all activity in December 2022 following the collapse of the Terra ecosystem in May 2022. The shutdown was a direct consequence of TerraUSD (UST) losing its dollar peg - since UST served as the primary collateral for all mAsset CDPs, its collapse effectively made the protocol insolvent. As of 2026, there is no active Mirror Protocol instance, and mAssets are no longer tradeable through the original platform.

Why did Mirror Protocol shut down?

Mirror Protocol shut down because its collateral base - TerraUSD (UST) - collapsed. UST was an algorithmic stablecoin whose peg relied on demand for LUNA, Terra's native token. In May 2022, UST began losing its dollar peg, triggering a death spiral: LUNA's price crashed trying to absorb UST redemptions, which destroyed UST's value further. Since all mAsset CDPs on Mirror were collateralized with UST, the protocol became insolvent when UST's value collapsed. Mirror officially ceased operations in December 2022.

What is the MIR token used for?

The MIR token served two functions in Mirror Protocol: governance and reward distribution. Governance: MIR holders staked tokens to vote on protocol proposals - whitelisting new mAssets, adjusting collateral ratios, changing fees, and allocating community pool funds. Reward distribution: every CDP closure generated a 1.5% fee on collateral, which was used to buy MIR on Terraswap and distribute to MIR stakers. This created a direct link between platform activity and staker returns. The total planned supply was approximately 370-375 million MIR, with no team allocation.

What are the best alternatives to Mirror Protocol in 2026?

For synthetic asset exposure, Synthetix on Ethereum and Optimism remains the most direct successor - permissionless, on-chain synthetics with a shared debt pool model rather than individual CDPs. For derivatives-based price exposure without CDP management, dYdX's perpetuals exchange on its dedicated Cosmos chain offers deep liquidity and a professional trading interface. For directly asset-backed tokenized stocks and Treasuries, Ondo Finance and Backed Finance provide regulated alternatives with hard asset backing rather than algorithmic collateral. Each carries different tradeoffs on access, collateral model, and regulatory structure.