Decentralized finance doesn't function without liquidity providers. They're the backbone of every DEX, every swap, every on-chain trade - and understanding how they work is essential if you're serious about DeFi.

This guide covers everything: what a liquidity provider actually is, how LP tokens work, what you earn, what risks you take on, and how to pick pools that match your risk profile. Whether you're evaluating your first liquidity position or looking to optimize an existing strategy, the mechanics covered here apply.

⚡ Key Takeaways

- Liquidity providers deposit crypto assets into smart contract-managed pools to enable decentralized trading

- In return, LPs receive LP tokens representing their proportional share of the pool

- LPs earn a share of every trading fee generated by the pool, proportional to their ownership percentage

- Impermanent loss is the primary structural risk - it occurs when deposited token prices diverge

- Anyone with a self-custody wallet can become a liquidity provider permissionlessly, with no approval required

What Is a Liquidity Provider in DeFi?

A liquidity provider is someone who deposits crypto assets into a smart contract-managed pool to enable token swaps on a decentralized exchange. Instead of waiting for a matching buyer or seller, traders swap directly against these pre-funded pools. LPs make that possible - and earn a cut of every trade that flows through.

To understand why LPs are necessary, you need to contrast two different market structures.

Traditional exchanges rely on an order book - a live ledger of limit orders from buyers and sellers. For a trade to execute, a willing counterparty must exist at the right price at the right time. In DeFi, there's no central authority to manage that matching process. Smart contracts handle execution, but they need pre-funded asset pools to fulfill swap orders. That's exactly the gap liquidity providers fill.

In return for depositing assets, LPs earn a share of the trading fees generated whenever someone swaps against their pool. On most automated market makers, that fee ranges from 0.01% to 1% per trade, depending on the pool tier.

How Automated Market Makers (AMMs) Work

Automated market makers are the algorithmic engine that prices assets within liquidity pools. Rather than relying on order books, AMMs use a mathematical formula to determine how much of token B a trader receives for depositing token A.

The most common model is the constant product formula, pioneered by Uniswap:

Here's how that plays out in practice. A pool holds 10 ETH and 20,000 USDC (k = 200,000). A trader buys 1 ETH.

📊 Worked Example: How AMM Pricing Shifts

Before trade: 10 ETH . 20,000 USDC = 200,000 (k)

After trade: pool must still equal 200,000

New state: 9 ETH → 200,000 ÷ 9 = ~22,222 USDC

Trader pays ~2,222 USDC for 1 ETH (effective price: $2,222 vs starting $2,000)

That price increase is not a bug - it's deliberate. As a token's supply in the pool decreases, the formula makes it progressively more expensive. This prevents pool drain and reflects basic supply/demand dynamics.

Different protocols optimize the formula for different use cases. Curve Finance uses a modified formula (the "stableswap invariant") that keeps prices near 1:1 between correlated assets, making it highly efficient for stablecoin pairs. Balancer supports pools with up to eight assets in customizable weightings, expanding well beyond the standard 50/50 split.

What Are LP Tokens and How Do They Work?

When you deposit assets into a liquidity pool, the protocol mints LP tokens and assigns them to you. These tokens are your receipt - they represent your proportional ownership of the pool's total assets.

LP tokens are fungible and freely transferable. You can trade them, transfer them to another wallet, or use them as collateral in other DeFi protocols. When you're ready to exit, you burn your LP tokens - the smart contract releases your proportional share of the pool's current assets, plus all accrued trading fees.

The full LP lifecycle looks like this:

- Deposit tokens → contribute equal value of both tokens in the pair

- Receive LP tokens → minted proportionally to your pool share

- Earn trading fees → accrue automatically as trades flow through the pool

- Stake for extra yield (optional) → deposit LP tokens into yield farming protocols for bonus rewards

- Burn LP tokens to exit → redeem your share of underlying assets + fees

LP tokens also unlock a strategy called yield farming: staking your LP tokens in additional protocols to earn governance tokens or supplemental yield on top of base trading fees. This stacking of returns is one of DeFi's most powerful compounding mechanisms - though it also compounds risk.

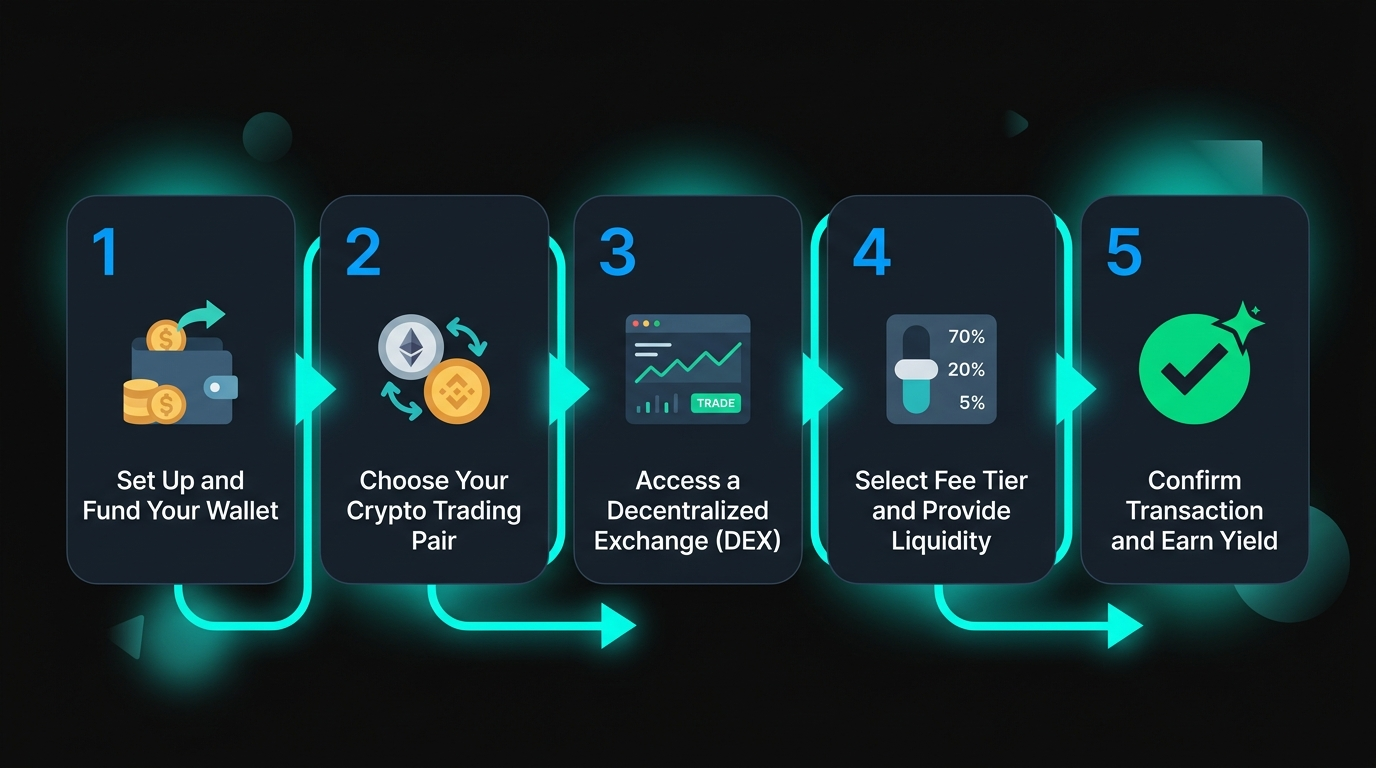

How to Become a Liquidity Provider: Step-by-Step

The process is permissionless. No KYC, no application, no minimum deposit requirements beyond what's practical given gas costs. Here's a concrete walkthrough.

Step 1: Choose Your Platform

Step 2: Set Up a Compatible Wallet

You'll need a self-custody wallet that supports the chain you're targeting. MetaMask covers Ethereum and EVM-compatible chains. Phantom handles Solana. Both can be connected directly to DEX interfaces without transferring custody of your assets.

Step 3: Fund Your Wallet

Acquire both tokens in the pair you want to provide liquidity for. On a standard AMM, you deposit equal dollar value of both tokens. If ETH is $3,000 and you want to deposit $2,000 total into an ETH/USDC pool, you'd need $1,000 worth of ETH (~0.333 ETH) and $1,000 USDC.

Step 4: Select a Pool and Fee Tier

On Uniswap V3, the same token pair may have multiple pools at different fee tiers: 0.01%, 0.05%, 0.3%, or 1%. Lower fees suit stable pairs with tight price correlation (USDC/USDT). Higher fees compensate LPs in volatile pairs where impermanent loss risk is higher.

Step 5: Set Your Position and Confirm

For standard AMMs (Uniswap V2, PancakeSwap), deposit and receive LP tokens in one transaction. For Uniswap V3, you'll also define a price range for your concentrated liquidity position (covered in the advanced strategies section below).

A note on gas fees: Ethereum mainnet transactions can cost $10-50+ during congestion. For smaller positions (under $5,000), Layer 2 networks like Arbitrum, Optimism, or Base offer the same Uniswap interface with fees under $0.10 per transaction.

Before committing capital, understand both the earning potential and the risks you're taking on.

Liquidity Provider Rewards and Risks

LP participation carries real earning potential. It also carries risks that aren't always obvious to first-time providers. Both sides of this equation deserve honest treatment.

Trading Fees and Yield Farming Opportunities

Every swap that flows through a pool generates fee income, distributed proportionally to LPs based on pool ownership. Here's what that looks like in practice:

📊 Fee Income Calculation: ETH/USDC Pool

Pool: ETH/USDC on Uniswap V3 (0.05% fee tier)

Daily trading volume: $5,000,000

Daily fee revenue: $5,000,000 . 0.0005 = $2,500

If you own 2% of the pool - daily earnings = $50

Monthly earnings ≈ $1,500

Annual fee APY on a $100,000 position ≈ 18%

These numbers fluctuate significantly based on pool volume, your pool share, and the fee tier. High-volume pools generate more fees; low-volume pools may not justify the IL exposure.

Beyond base fee income, many protocols offer yield farming incentives: deposit your LP tokens into a staking contract and earn additional governance tokens. On top of trading fees, this can meaningfully boost total APY - though these reward tokens often carry inflation risk and may depreciate over time. Always distinguish between fee-based yield (sustainable) and token-emission yield (potentially inflationary). For a deep dive on how yield aggregators compound these returns automatically, see Yearn Finance explained.

Impermanent Loss Explained

Impermanent loss is the most misunderstood concept in LP participation - and the most important one to understand before depositing anything.

The mechanism: When you deposit into a pool, the AMM's constant product formula continuously rebalances your holdings as prices change. If one token appreciates significantly, the pool automatically sells some of it for the other token to maintain the formula. You end up holding more of the depreciating asset and less of the appreciating one - compared to simply holding both tokens in your wallet.

Here's a concrete example with real numbers:

The "impermanent" qualifier is precise: if ETH returns to $3,000 before you withdraw, the loss disappears entirely. It only becomes realized at the moment of withdrawal when prices have diverged. Fee income offsets this loss - in high-volume pools, fees can exceed IL and result in net profit even with significant price divergence.

Minimizing IL: The most straightforward approach is choosing pairs with low price correlation - stablecoin pairs (USDC/USDT on Curve Finance) experience near-zero IL because the prices don't diverge. Liquid staking token pairs (wstETH/ETH) also minimize IL because both assets track ETH closely. Impermanent loss calculators (available on DeFiLlama and DailyDeFi) let you model IL scenarios before depositing.

How to Choose the Right Liquidity Pool: Evaluation Framework

Choosing the wrong pool is one of the most common LP mistakes. Here's the framework I use when evaluating any new position.

Key Pool Metrics Every LP Should Track

Once you're in a pool, monitoring these metrics helps you decide when to exit or rebalance:

- ✓ TVL - pool depth; declining TVL can signal LP exits and impending low-liquidity issues

- ✓ 24h Trading Volume - fee income driver; track via DeFiLlama or Uniswap Analytics

- ✓ Fee APY vs Incentive APY - separate base yield from subsidized yield

- ✓ Your IL vs Fee Accumulation - net position performance; impermanent loss calculators help

- ✓ Smart Contract Audit Status - always verify before new deposits

Free tools: DeFiLlama (TVL tracking across all chains), Uniswap Info (Uniswap-specific pool analytics), Dune Analytics (custom on-chain dashboards). For IL tracking, both CoinGecko and DailyDeFi offer dedicated calculators.

Risks and Red Flags in DeFi Liquidity Provision

Impermanent loss gets most of the attention - but it's not the only risk. Several others can be more severe.

⚠ Red Flags Before Depositing into Any Pool

- No audit → by a reputable firm (Certik, Trail of Bits, OpenZeppelin, Chainalysis)

- Anonymous team + new token → no public accountability, highest rug pull risk

- APY exceeding 500% → almost always unsustainable token emissions

- Reward token with no utility → no market outside the protocol

- Admin keys not renounced → or protected by a time-lock contract

Smart contract exploits are the most severe risk - and the most binary. A single vulnerability in pool code can drain all funds permanently. Established protocols like Uniswap, Curve, and Aave have undergone multiple independent audits and years of battle-testing. New forks launching with modified code often skip this process. The risk premium for unaudited protocols is not compensated by even exceptional APY.

Rug pulls target LPs specifically. A malicious project creates a token, bootstraps a liquidity pool with inflated incentives, and attracts LP deposits - then the team drains the pool or dumps the token, leaving LPs holding a worthless asset. Before depositing into any new project, check whether liquidity is locked via a time-lock contract and whether the team is publicly accountable.

Token depeg risk is particularly relevant in stablecoin pools. If one stablecoin in a pair loses its peg (as USDC briefly did in March 2023 and UST catastrophically did in 2022), LP positions absorb the full divergence as impermanent loss that can crystallize instantly into permanent loss.

Inflationary reward tokens are a subtler risk. A pool advertising 300% APY where 280% comes from emissions of a newly minted governance token often looks very different six months later when that token has lost 90% of its value. Always decompose the APY: fee-based component (sustainable) vs emission-based component (potentially worthless).

Advanced LP Strategies: Maximizing Returns While Managing Risk

Standard AMM participation is straightforward but capital-inefficient. If you're providing liquidity across the full price range (0 to infinity), most of your capital sits idle while trades happen in a narrow range around the current price. Concentrated liquidity changes that equation.

Concentrated Liquidity: Earning More With Less Capital

Uniswap V3 introduced concentrated liquidity in 2021, fundamentally changing the capital efficiency of LP participation. Instead of distributing capital across all possible prices from zero to infinity, you define a specific price range within which your capital is deployed.

The tradeoff: if ETH price moves outside your defined range, your position stops earning fees entirely. You're holding 100% of the weaker asset at that point, waiting for price to re-enter your range. This requires active monitoring and periodic rebalancing.

For LPs who want concentrated liquidity benefits without constant management, automated range management tools - Gamma Strategies, Arrakis Finance, and Beefy's managed vaults - handle rebalancing algorithmically. These services charge a management fee but remove the manual overhead.

Alternatives to Providing Liquidity Directly

Direct LP participation isn't the only path to DeFi yield. For those who want on-chain returns without the complexity and risk profile of liquidity provision, several alternatives exist.

Lending protocols like Aave and Compound let you deposit a single asset - ETH, USDC, WBTC - and earn interest from borrowers, with no impermanent loss exposure. Yields are lower than LP participation in high-volume pools, but the risk profile is cleaner.

Yield aggregators like Yearn Finance and Beefy automate complex LP strategies and compound returns continuously. You deposit an asset, the vault handles pool selection and rebalancing, and you earn a net yield after management fees. This is the closest thing to truly passive DeFi yield.

Liquid staking issues you a receipt token (stETH from Lido, rETH from Rocket Pool) representing staked ETH earning validator rewards. You can then use these LSTs in DeFi - as collateral, in Curve pools - without losing access to your underlying yield. No IL, no pool management, just protocol-level ETH yield.

Direct LP provides the highest potential yield and the most control, but demands more active management and carries structural risks that these alternatives avoid. The right choice depends on your risk tolerance, capital size, and time available for monitoring.

Conclusion

Liquidity providers are the infrastructure layer that makes decentralized trading possible. Without LPs depositing assets into smart-contract-managed pools, DEXs can't execute swaps, traders can't access on-chain markets, and the permissionless financial system doesn't function. Understanding this role - and executing it well - is one of the highest-leverage skills in DeFi.

The core mechanics are now clear: deposit tokens, receive LP tokens representing your pool share, earn trading fees proportional to your contribution, and redeem your position by burning LP tokens. The constant product formula governs pricing; impermanent loss is the structural tradeoff for that liquidity provision.

The direction of DeFi liquidity is toward greater capital efficiency. Uniswap V4's hook architecture, cross-chain liquidity via protocols like LayerZero, and IL protection mechanisms from projects like Bunni are reshaping what LP participation looks like. As on-chain infrastructure matures, the gap between passive holding and active liquidity provision is closing - particularly on platforms built around real yield mechanics rather than inflationary token emissions.

For traders and DeFi participants who want LP exposure within a platform that generates real protocol revenue from actual trading and market activity - rather than emissions-based APY - it's worth exploring platforms where fee revenue flows directly to liquidity providers on-chain. Zipmex is built on exactly that model: real yield from platform fees, on-chain verifiable mechanics, full self-custody. The trend in DeFi is moving toward that standard.

Crypto trading and liquidity provision involve substantial risk of loss. Liquidity pools expose participants to smart contract risk, impermanent loss, and market volatility. This article is for informational purposes only and does not constitute financial advice. Assess your own risk tolerance before providing liquidity in any DeFi protocol.

Last updated: April 2026.

Frequently Asked Questions

What is a liquidity provider in crypto?

A liquidity provider in crypto is someone who deposits assets into a decentralized exchange's smart-contract-managed liquidity pool to enable token trading. Instead of matching buyers and sellers through an order book, DEXs use these pre-funded pools to fulfill swap orders algorithmically. In return for supplying assets, LPs receive LP tokens representing their pool ownership share and earn a proportional cut of every trading fee generated by the pool. Anyone with a self-custody wallet can become a liquidity provider without permission, approval, or minimum deposit requirements beyond practical gas cost considerations.

What is impermanent loss and how does it affect LPs?

Impermanent loss (IL) occurs when the price of tokens you deposited into a pool diverges from their prices at the time of deposit. Because AMM formulas continuously rebalance pool ratios, LPs end up holding more of the depreciating token and less of the appreciating one compared to simply holding. If you deposit 1 ETH and 3,000 USDC when ETH is $3,000 and ETH doubles to $6,000, your pool position is worth roughly $8,485 vs $9,000 if you'd just held - a ~$515 impermanent loss. The "impermanent" qualifier applies because if prices return to original levels before withdrawal, the loss vanishes entirely.

How do liquidity providers make money in DeFi?

LPs earn primarily through trading fees - a small percentage of each swap that flows through their pool, distributed proportionally to all LPs based on pool ownership. On most AMMs, fees range from 0.01% to 1% per trade. On a pool generating $5,000,000 in daily volume with a 0.3% fee, a 1% pool share earns roughly $150/day in fee income. Beyond base fees, many protocols offer additional yield farming incentives - staking LP tokens in governance contracts to earn bonus token rewards. Fee-based income is sustainable; emission-based incentives require closer scrutiny.

What are LP tokens and what can I do with them?

LP tokens are receipt tokens issued when you deposit into a liquidity pool - they represent your proportional ownership of that pool's total assets. Their value equals pool TVL divided by the circulating LP token supply. You can hold them to accumulate trading fee income, stake them in yield farming protocols to earn bonus governance token rewards, use them as collateral in lending platforms like Aave, or transfer them to another wallet. To exit the pool, you burn your LP tokens - the smart contract releases your proportional share of the pool's current assets plus all accrued fees.

What is an automated market maker (AMM)?

An automated market maker is a smart contract protocol that prices and executes token swaps algorithmically, without order books or human market makers. AMMs use mathematical formulas to determine prices based on the ratio of tokens held in their liquidity pools. The most common formula is the constant product model (x * y = k), where k stays constant and prices adjust automatically as traders swap tokens. Uniswap popularized this model; Curve modified it for stablecoin efficiency; Balancer extended it to multi-token weighted pools. AMMs are the core infrastructure of every major DEX and make permissionless, always-available trading possible in DeFi.

What is concentrated liquidity in Uniswap V3?

Concentrated liquidity, introduced in Uniswap V3, allows LPs to deploy capital within a specific price range rather than across all possible prices. If ETH trades at $3,000 and you concentrate liquidity in a $2,700-$3,300 range (±10%), your capital earns fees only when ETH trades within that range - but earns them at dramatically higher efficiency than standard AMM deployment. Capital efficiency gains can be 10x-50x compared to V2 equivalents, depending on range width. The tradeoff: if price moves outside your range, your position stops earning fees and holds 100% of the weaker asset. Active range management or automated vaults via Gamma or Arrakis are required to maintain fee income over time.

Can I lose money as a liquidity provider?

Yes - LP participation carries multiple loss vectors. Impermanent loss means your position can underperform simply holding the assets if token prices diverge significantly. Smart contract exploits can result in total loss if pool code contains vulnerabilities. Token collapse (depeg, rug pull, or fundamental project failure) permanently crystallizes losses. And inflationary reward tokens offered as yield farming bonuses may depreciate faster than they accumulate. The probability of significant loss can be reduced by focusing on established, audited protocols with blue-chip or correlated token pairs - but no DeFi activity carries zero risk. Always deploy only capital you're prepared to lose entirely.