You see a price. You click buy. The trade confirms - and the number is different. That gap has a name: slippage. It's one of the most common hidden costs in crypto trading, and most traders don't realize how much it's costing them until they start paying attention.

⚡ Quick Answer

Slippage in crypto is the difference between the price you expected when placing a trade and the price at which it actually executes. It happens because crypto markets move continuously - by the time your order reaches the market, the price may have shifted. Slippage can work in your favor (positive) or against you (negative), and it's more pronounced on DEXs, during high volatility, and when trading low-liquidity assets.

What Is Slippage in Crypto?

Slippage in crypto is the discrepancy between the expected execution price and the actual execution price of a trade. It occurs in every type of financial market, but it's especially pronounced in crypto due to the asset class's well known volatility and the fragmented liquidity across hundreds of exchanges.

Think of it like this: you walk up to a market stall with a price tag of $50 on an item. But by the time you hand over the cash, the price has changed to $52. In crypto, that $2 difference is slippage - and it compounds fast when you're trading larger sizes or less liquid assets.

According to research cited by SEI, aggregate slippage costs across crypto markets exceeded $2.7 billion in 2024 - a 34% increase from the previous year. That's not an abstract number. It represents real losses borne by traders who didn't account for execution gaps.

🎯 Key Takeaways

- Slippage is the gap between your expected price and your actual execution price

- It can be positive (better price) or negative (worse price) - though negative is more common

- Market orders are far more vulnerable to slippage than limit orders

- DEXs expose you to unique slippage risks including sandwich attacks from MEV bots

- You can calculate slippage using: ((Executed Price - Expected Price) / Expected Price) . 100

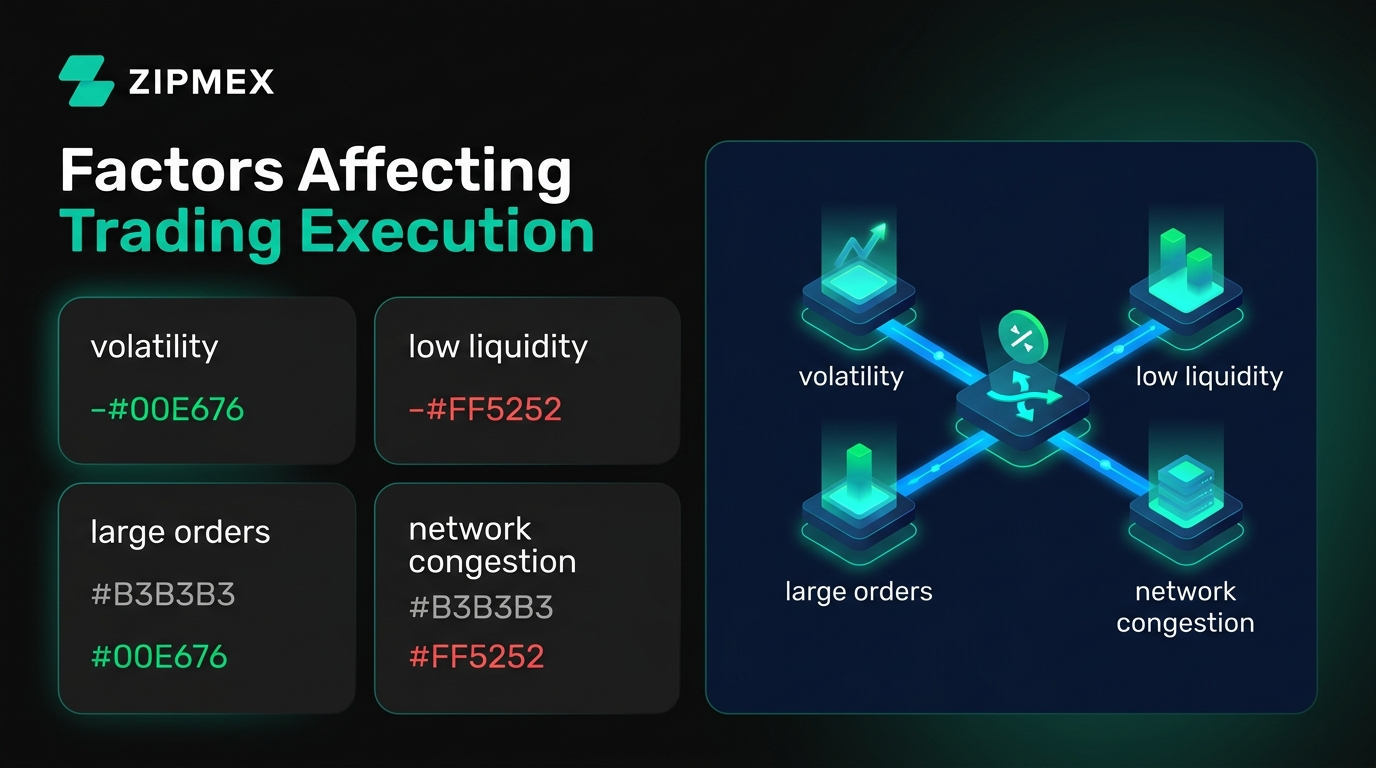

What Causes Slippage in Crypto?

Understanding why slippage happens is the first step to controlling it. There are four primary causes - and they often combine to make things worse at the worst possible moments.

Market Volatility

Crypto markets move fast. Prices can shift by a meaningful percentage in seconds during news events, large liquidations, or sudden shifts in sentiment. When prices move rapidly between the moment you place an order and the moment it executes, you get slippage. The faster and more unpredictably prices move, the larger the gap.

This innate latency window is a foundational characteristic of shared infrastructure, where global network states must achieve cryptographic consensus across independent operators before updating the ledger. Developing a firm grasp on how nodes record data cryptographically and secure sequential transaction strings is crucial for predicting price tolerance zones. For a deep technical exploration of this distributed network architecture, follow our comprehensive manual on what are blockchains and how do distributed ledgers work.

Low Liquidity

Liquidity refers to how easily an asset can be bought or sold without affecting its price. In a liquid market, there are enough buyers and sellers at various price levels that large orders fill near the expected price. In a low-liquidity environment - think a newly launched altcoin or a trading pair with few active participants - your order "eats through" the order book, matching with progressively worse prices until it's filled.

Large Order Size

Even in a moderately liquid market, a very large order can trigger slippage. If you're buying a significant amount of a token, you'll exhaust the available orders at the best price and continue filling at worse levels. This is sometimes called price impact, and it's especially visible in smaller-cap tokens.

Network Congestion

On decentralized exchanges, your transaction must be confirmed on-chain before it executes. During periods of high network congestion, confirmation times increase - and prices can move significantly in the window between you signing the transaction and it being processed. This is a uniquely crypto problem that doesn't exist on traditional centralized order books.

⚠ Risk Warning

During major news events or market crashes, all four causes of slippage can activate simultaneously - volatility spikes, liquidity drains, large orders flood the market, and networks congest. This is when slippage costs are highest, and it's exactly when traders are most likely to be placing urgent market orders.

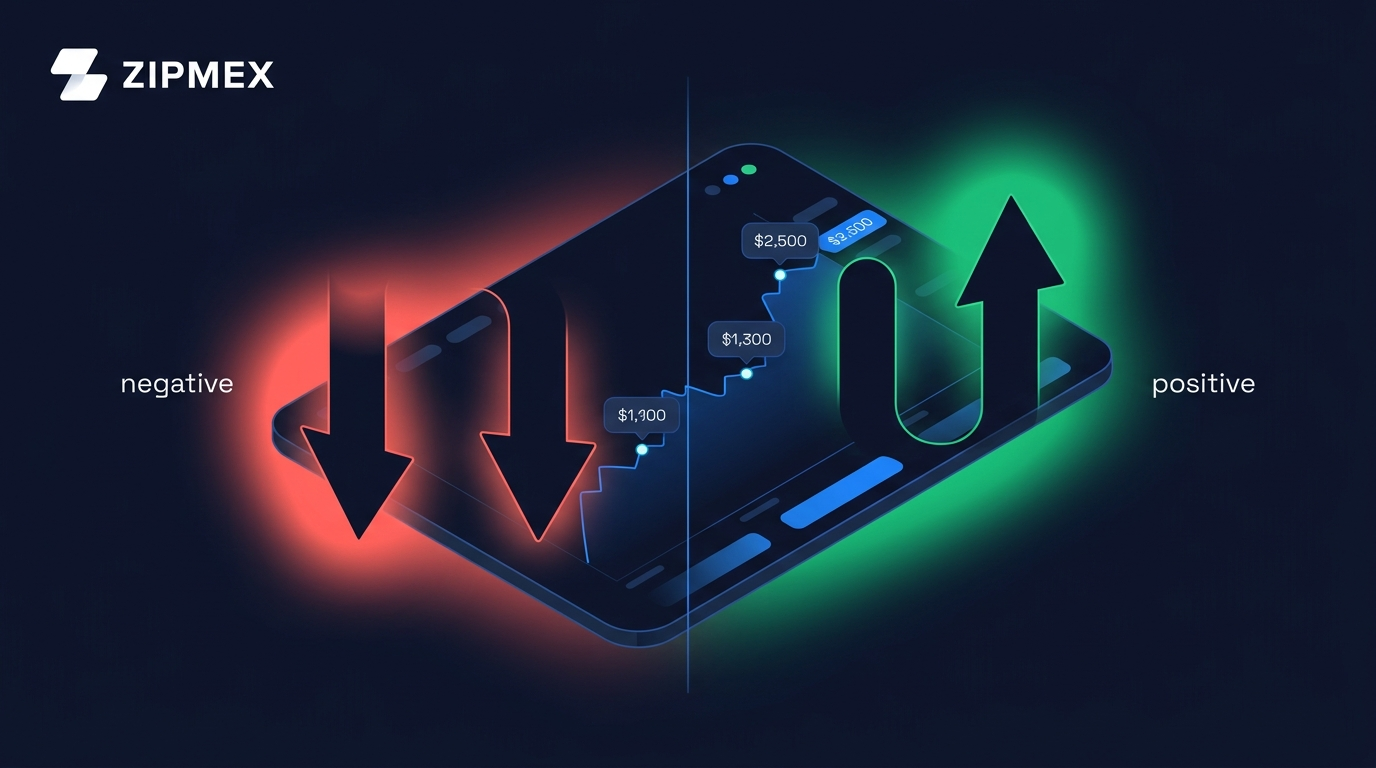

Positive vs Negative Slippage

Not all slippage is bad. There are two directions it can go, and understanding both helps you react calmly when it happens.

Negative Slippage

This is the type most traders encounter and dislike. Negative slippage occurs when your trade executes at a worse price than expected. If you place a buy order expecting to pay $2,000 per ETH and your order fills at $2,020, you've experienced $20 of negative slippage - a 1% execution gap.

Negative slippage effectively increases the cost of buying and decreases the proceeds from selling. Over many trades, it accumulates into a meaningful drag on returns.

Positive Slippage

Positive slippage occurs when your trade executes at a better price than expected. Using the same example: you expect to buy at $2,000 but the order fills at $1,985. You've saved $15 per ETH.

Positive slippage is real and does happen - particularly when selling into strong buying pressure, or when a market order catches a brief liquidity surge. It's less common than negative slippage in volatile conditions, but it's worth knowing it exists.

How to Calculate Slippage

You can measure the slippage on any completed trade using this formula:

Slippage % = ((Executed Price - Expected Price) / Expected Price) . 100

For example: if you expected to buy 1 SOL at $130 but it filled at $133.90, your slippage is:

((133.90 - 130) / 130) . 100 = 3% slippage

That percentage tells you exactly how far execution drifted from your expectation - and whether it's within an acceptable range for your strategy.

What Is Slippage Tolerance?

Slippage tolerance is the maximum deviation from your expected price that you're willing to accept before a trade is automatically cancelled. It's a protective setting that prevents you from getting an execution wildly different from what you intended.

On most decentralized exchanges and many centralized platforms, you can set your slippage tolerance as a percentage. Here's how it works:

- If you set 0.5% tolerance and the price moves more than 0.5% before your transaction confirms, the swap is automatically reverted. You get your tokens back (minus gas fees on DEXs).

- If you set 5% tolerance, the transaction will proceed even if the price moves up to 5% against you - which can be very costly.

Recommended Slippage Tolerance Settings

The right tolerance depends on what you're trading and where:

Setting tolerance too tight causes failed transactions and wasted gas. Setting it too loose exposes you to excessive costs - and, on DEXs, to a specific type of attack called a sandwich attack.

The Sandwich Attack Problem

On public blockchains, your pending swap transaction sits in the mempool - visible to anyone before it confirms. MEV (Maximal Extractable Value) bots watch this mempool constantly. When they detect a large swap with a loose slippage tolerance, they execute a deliberate sequence: buy the token just before your transaction, push the price up, let your trade fill at the inflated price, then sell immediately after - pocketing the difference as profit.

This is why setting a high slippage tolerance on a DEX isn't just costly - it actively signals to bots that your trade is worth attacking.

How to Reduce Slippage in Crypto Trading

You can't eliminate slippage entirely - but you can minimize it significantly with the right habits. Here are seven strategies that actually work.

Use Limit Orders Instead of Market Orders

Market orders execute immediately at whatever price is available - making them highly vulnerable to slippage. Limit orders execute only at your specified price or better, giving you full control over your execution cost. Understanding the difference between maker and taker orders is foundational here: limit orders make you a maker and typically save you both on slippage and fees.

Trade During High-Liquidity Windows

Liquidity peaks when the US and European trading sessions overlap (roughly 8am-12pm EST). During these hours, narrower bid-ask spreads and higher order book depth reduce slippage for most pairs. Avoid trading immediately after major news announcements, when volatility spikes and liquidity drains.

Split Large Orders Into Smaller Chunks

If you're moving a large position, breaking it into smaller orders over time reduces your price impact. This approach - known as TWAP (Time-Weighted Average Price) execution - is standard practice for institutional traders and is worth adopting for significant retail trades too.

Set a Conservative Slippage Tolerance on DEXs

As covered above, keeping your DEX tolerance at 0.5-1% for major pairs dramatically reduces your exposure to sandwich attacks while still ensuring most trades execute. Treat any setting above 3% as a last resort for genuinely illiquid tokens.

Use DEX Aggregators for Better Routing

Platforms like 1inch and Matcha automatically route your trade across multiple liquidity sources to find the best execution price. For tokens available across several pools, aggregators consistently deliver lower slippage than trading directly on a single DEX - particularly for larger orders.

Trade High-Liquidity Pairs When Possible

BTC/USDT and ETH/USDC have the deepest order books in crypto. If your strategy allows, routing through these major pairs (even as an intermediate step) typically results in lower slippage than trading directly into a low-cap token. Check market depth before entering - shallow order books are a clear slippage warning sign.

Consider OTC Desks for Very Large Trades

For trades exceeding $100,000, OTC (Over-The-Counter) desks offer fixed-price execution that bypasses public order books entirely - eliminating slippage risk. Major exchanges like Binance, Kraken, and Coinbase all offer OTC services, typically with no minimum fees and competitive pricing for qualified traders.

Your signal won't wait for KYC

Connect wallet, open a perp in 30 seconds on ZEXO. No email, no ID, no account.

Trade on ZEXO →To completely avoid the volatile latency and unpredictable mainnet fees that directly cause transaction delays, professional on-chain traders frequently migrate their activities to high-throughput layer-2 environments. Utilizing these advanced rollup architectures compresses transaction processing times down to fractions of a second, which shields your trade entries from unexpected price drift. You can explore how these throughput multipliers optimize asset efficiency in our specialized guide on what is Arbitrum (ARB) and how it scales the Ethereum ecosystem.

Slippage on CEX vs DEX: Key Differences

The mechanics of slippage differ meaningfully between centralized and decentralized exchanges. Understanding both helps you calibrate your expectations and strategies for each environment.

On a CEX, market makers provide continuous liquidity and keep spreads tight. The order book matching is fast, and for most retail trade sizes, slippage on major pairs is negligible. On a DEX, you're trading against automated market maker pools - algorithmic contracts where the price is determined by the ratio of tokens in the pool. Every trade shifts that ratio slightly, causing price impact proportional to your order size relative to pool depth.

Shifting your trade execution away from centralized brokers onto these peer-to-peer liquidity networks completely alters the rules of capital routing and price discovery. Because decentralized platforms resolve transactions entirely via transparent smart contracts rather than matching desks behind closed doors, mastering pool mechanics is essential for preventing structural losses. To explore the technical foundations of these non-custodial trading environments, check out our master overview on what is a DEX and how decentralized exchanges work.

For most crypto traders, CEXs offer materially lower slippage for standard trades. DEXs trade that efficiency for permissionlessness and access to assets that never appear on centralized platforms.

It's also worth noting how slippage connects to crypto arbitrage: price gaps between CEXs and DEXs that create arbitrage opportunities are often partially driven by slippage costs, liquidity imbalances, and different fee structures across platforms.

Frequently Asked Questions

What is slippage in crypto in simple terms?

Slippage is the difference between the price you see when placing a trade and the price your trade actually executes at. It happens because crypto prices move constantly, and by the time your order reaches the market, the price may have shifted. Think of it as the "cost of immediacy" when using market orders.

Is slippage always bad?

No. Slippage can be positive (you get a better price than expected) or negative (you get a worse price). Positive slippage happens when the market moves in your favor during execution. However, negative slippage is more common, especially during volatile markets or when trading less liquid assets.

What is a good slippage tolerance for crypto?

For major pairs like BTC/USDT or ETH/USDC, 0.1%-0.5% is appropriate. For mid-cap tokens, 0.5%-1% works well. For smaller altcoins, you may need 1%-3%. Avoid setting tolerance above 3-5% as it significantly increases your risk of sandwich attacks on DEXs.

Why does slippage happen more on DEXs?

DEXs use automated market maker (AMM) pools rather than traditional order books. In an AMM, every trade shifts the token ratio in the pool, directly impacting the price. Additionally, DEX transactions must be confirmed on-chain, which takes time - during which the price can move further. Finally, DEXs are vulnerable to MEV bots that specifically target trades with loose slippage settings.

Can I avoid slippage completely?

Not entirely. But you can minimize it significantly by using limit orders on CEXs, setting a conservative slippage tolerance on DEXs, trading during high-liquidity periods, splitting large orders, and using DEX aggregators. For very large trades, OTC desks offer fixed-price execution with zero slippage risk.

How do I calculate slippage percentage?

Use this formula: ((Executed Price - Expected Price) / Expected Price) . 100. For example, if you expected $130 per SOL but paid $133.90, your slippage is ((133.90 - 130) / 130) . 100 = 3%.

Does slippage affect all cryptocurrencies equally?

No. Bitcoin and Ethereum on major exchanges experience the least slippage due to deep liquidity. Smaller altcoins, newly launched tokens, and tokens on low-liquidity DEX pools experience much more slippage - sometimes 5-20%+ for larger trades. Always check market depth before placing a significant order on a less-known pair.

Conclusion

Slippage in crypto is an unavoidable reality of trading in fast-moving, fragmented markets. But "unavoidable" doesn't mean "unmanageable." The difference between traders who account for slippage and those who don't shows up consistently in their results over time.

The core principles are straightforward: prefer limit orders over market orders, keep your DEX slippage tolerance conservative, trade when liquidity is deep, and understand that what you see on your screen and what you pay aren't always the same number.

The more you understand how execution actually works - across both CEXs and DEXs - the better positioned you are to control your trading costs and make your strategy work as intended.

Stop depositing. Start trading.

ZEXO perps execute straight from your wallet. No deposits, no withdrawals, no waiting.

Open ZEXO →⚠ Disclaimer: The information provided in this article is not intended to provide investment or financial advice. Investment decisions should be based on the individual's financial needs, objectives, and risk profile. We encourage readers to understand the assets and risks before making any investment entirely. Cryptocurrency investments are subject to high market risk. Past performance does not guarantee future results.