Every crypto trader has experienced it: you lock onto a price, hit buy, and the confirmation shows something slightly different. That gap - between the price you expected and the price you actually got - is slippage. It's one of the most common and least-discussed costs in crypto trading, and if you don't understand it, it will quietly drain your returns over time.

⚡ Key Takeaways

- Slippage is the difference between the expected and actual execution price of a crypto trade, expressed as a percentage.

- The main causes are market volatility, low liquidity, large order sizes, and - unique to crypto - blockchain network congestion.

- You can substantially reduce slippage by using limit orders on centralized exchanges and setting a sensible slippage tolerance on DEXs.

Let's start with the definition.

What Is Slippage in Crypto?

Slippage in crypto refers to the difference between the expected price of a trade and the price at which it actually executes. It applies to both buy and sell orders and is typically expressed as a percentage of the expected price. A 1% slippage on a $10,000 Bitcoin order means you paid $100 more - or received $100 less - than you planned.

This phenomenon exists in traditional markets too (forex, equities), but crypto amplifies it significantly. Extreme price volatility, thin liquidity on altcoin pairs, and the architectural quirks of decentralized exchanges all make slippage a more frequent and more costly problem than most new traders anticipate.

⚡ Definition

Slippage = the difference between the expected and actual execution price of a trade, expressed as a percentage.

How Does Slippage Work? The Mechanics Explained

Here's what's actually happening under the hood. When you place a market order to buy 1 ETH at $2,000, that order hits the exchange's order book and starts consuming available sell orders - the cheapest ones first. If 50 ETH are listed at $2,000 but another buyer snaps up 40 of them in the milliseconds before your order fills, your order has to consume the next available price level, say $2,020. You end up paying $2,020 for that ETH.

The formula for calculating slippage is:

That's $20 on a single ETH trade. Scale that across dozens of daily trades and the cumulative drag becomes significant.

Positive vs. Negative Slippage: Not Always a Loss

Most traders only think about slippage when it hurts them - but it actually cuts both ways.

Negative slippage is far more common - especially during volatile conditions where prices move against you between order placement and execution. One nuance worth knowing: some centralized exchanges retain positive slippage rather than passing it back to the trader. If you're consistently getting the worst of both outcomes, check your platform's execution policy.

What Causes Slippage in Crypto?

Slippage doesn't happen randomly - it has four distinct causes, and they often compound. A large order placed during a news-driven price spike on a low-cap altcoin? That's a worst-case scenario where all four triggers fire at once.

Market Volatility

Crypto prices can move 5-10% in under a minute during major events - protocol hacks, macro announcements, exchange listings, even a single high-profile post. When price is moving that fast, the gap between your order price and your fill price can widen dramatically, even on trades that take less than a second to execute. Bitcoin's well-documented volatility makes it one of the most visible examples of this, though high-beta altcoins are considerably worse.

Low Market Liquidity

Liquidity is the availability of willing buyers and sellers at a given price. When it's thin, a large order has to "walk the book" - consuming progressively worse price levels to fill the entire order. Think of it like a street market with limited supply: you buy the first 10 units at $2 each, then 5 more at $3, then 3 at $5, because each vendor only had so many. Your average cost ends up far above what the listed price implied. In crypto, this plays out constantly on mid-cap and low-cap tokens where order book depth is shallow.

Large Order Size and Market Depth

Even on a high-liquidity exchange like Binance or Kraken, a sufficiently large order will exhaust the best available prices and cascade into worse levels. This is why institutional traders and high-net-worth individuals rarely hit the market with a single buy - more on the solution to that in the minimization section below.

Network Congestion and Transaction Delays

This one is unique to crypto. On decentralized exchanges built on Ethereum, your transaction doesn't execute the moment you submit it - it enters the mempool and waits for a validator to include it in a block. During high-congestion periods (NFT mints, DeFi launches, network stress events), that wait can stretch from seconds to minutes. The market keeps moving while your transaction sits pending, and when it finally executes, the price may have shifted substantially. Gas fee dynamics compound this further: higher fees get prioritized, meaning underbidding on gas during a busy period can leave your DEX swap in limbo at a stale price.

How to Calculate Slippage in Crypto

There's no mystery to the math. The formula is:

Slippage (%) = ((Executed Price - Expected Price) / Expected Price) . 100

A positive result means you overpaid on a buy order. A negative result on a sell order means you received less than expected. Either direction represents a real cost.

On DEXs, this percentage is exactly what you're configuring when you set your slippage tolerance - you're telling the protocol the maximum deviation you're willing to accept before the transaction reverts.

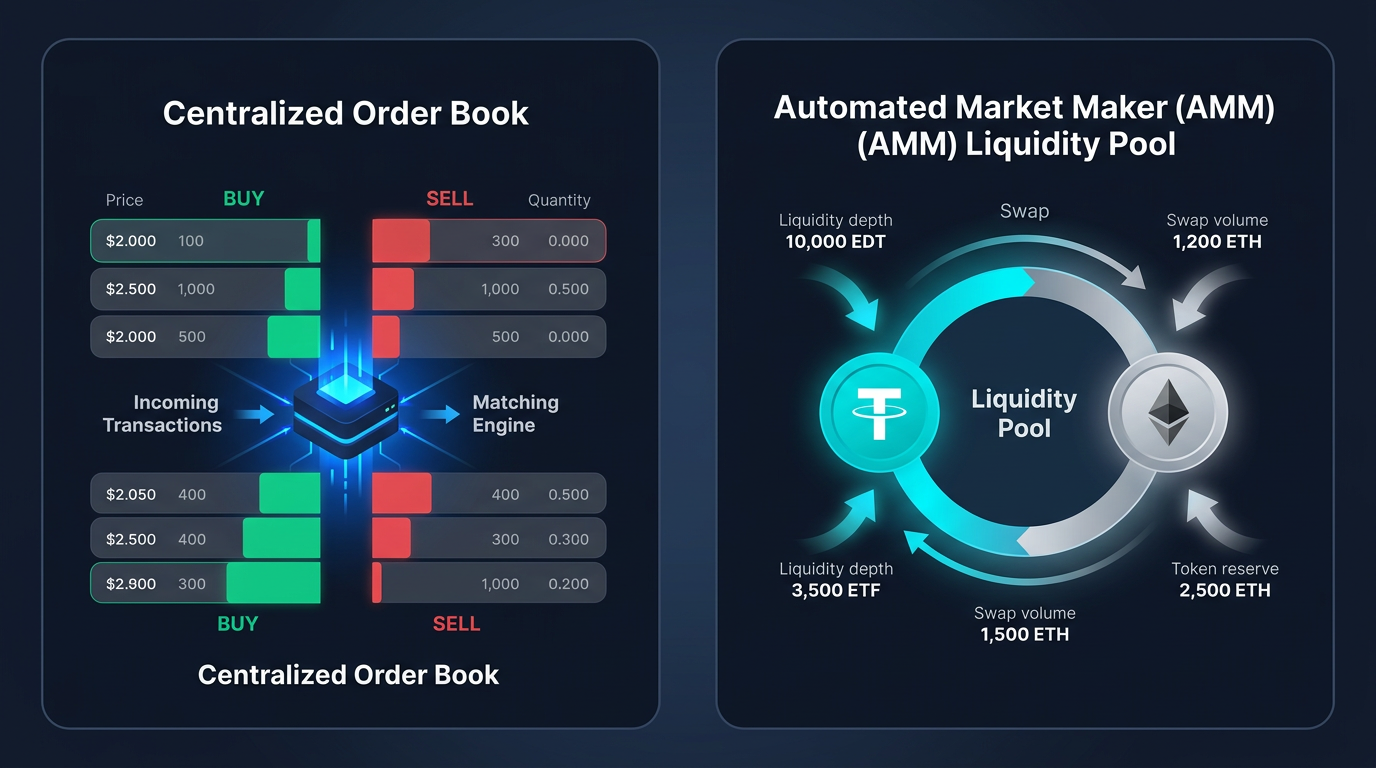

Slippage on CEX vs. DEX: Key Differences

Where you trade matters as much as how you trade. Centralized and decentralized exchanges handle slippage through fundamentally different mechanisms, and your exposure changes depending on the platform.

How Slippage Works on Centralized Exchanges

On CEXs - Binance, Kraken, Coinbase - trades execute against a centralized order book managed by the exchange. Market orders consume the cheapest available sell orders first and cascade to worse prices if depth is insufficient. The standard defense is a limit order: you specify an exact execution price, and the order only fills at that price or better, guaranteeing zero slippage. The trade-off is potential non-execution if the market moves away. For context, Kraken Pro surfaces a warning when projected slippage on a market order reaches 3% or more - a practical signal that your order size is straining available liquidity at your target price.

How Slippage Works on Decentralized Exchanges (AMMs)

DEXs like Uniswap don't use order books. They use Automated Market Makers (AMMs), where price is determined algorithmically by the ratio of assets in a liquidity pool. Every swap shifts that ratio, producing what's called price impact - which is the DEX equivalent of slippage. Larger swaps move the ratio more, creating larger price impact.

Before submitting a DEX transaction, you set a slippage tolerance - typically 0.1% to 5%. Set it too low and the transaction reverts if the price moves beyond your threshold. Set it too high and you become a target for MEV bots. The balance between execution certainty and MEV protection is something every serious DEX trader needs to calibrate.

Comparison: CEX vs. DEX Slippage

The Hidden Risks of High Slippage in Crypto

Beyond the obvious cost of a bad fill, slippage mismanagement carries two underappreciated risks that can do serious damage to active traders.

⚠ Risk Warning

- Setting slippage tolerance above 5% on DEXs → significantly increases exposure to MEV bots and sandwich attacks.

- Crypto trading involves substantial risk of loss → always understand the mechanics of the platform you're using before executing.

Frontrunning and MEV Bots Explained

MEV stands for Maximal Extractable Value - the profit that validators or sophisticated bots extract by reordering, inserting, or front-running transactions in the mempool before they're confirmed on-chain. According to Ethereum's documentation on MEV, this has become a structurally embedded feature of public blockchains, not a temporary edge case.

The most common MEV attack targeting retail traders is the sandwich attack:

SANDWICH ATTACK - HOW IT WORKS

Step 1

Bot detects your pending DEX swap in the mempool - you're buying Token X with high slippage tolerance.

Step 2

Bot front-runs your trade - buys Token X first, pushing the price up before your order fills.

Step 3 - You pay the price

Your trade executes at the inflated price - you fill at or near the top of your slippage tolerance.

Step 4

Bot immediately sells Token X - dumps into your buy pressure and pockets the margin difference.

The result: you paid the maximum price your tolerance allowed, and the bot extracted the margin. This isn't theoretical - sandwich attacks are documented, measurable, and ongoing on Ethereum-based DEXs. Keep DEX slippage tolerance at ≤1% for major pairs and ≤3% for mid-caps. Only exceed that when dealing with tokens with specific technical requirements, and understand you're accepting elevated MEV exposure.

At scale, even a routine 1-2% slippage per trade translates into thousands of dollars in annual drag for active traders - a silent performance killer that never shows up in a single trade's P&L but destroys long-run returns.

How to Minimize Slippage in Crypto Trading

The good news: with the right settings and habits, slippage is largely manageable. Here are four concrete techniques I rely on.

Use Limit Orders Instead of Market Orders

A limit order specifies the exact price at which you're willing to trade. The order only fills at that price or better - which means zero slippage by definition. The trade-off is that the order may not execute if the market moves away from your limit before it fills. For most non-time-sensitive trades on CEXs, limit orders are the obvious choice. Market orders still make sense on deep-liquidity major pairs (BTC/USDT, ETH/USDT) when execution speed matters more than precision entry.

Set a Sensible Slippage Tolerance on DEXs

This is the single highest-impact adjustment most DEX traders can make. Here are the thresholds I use:

The "Custom" tolerance field on most DEX interfaces (Uniswap, Curve, etc.) is where you enter these values directly. Defaulting to the auto-setting is fine for casual use, but optimizing tolerance by trade type is a habit that pays off.

Trade High-Liquidity Pairs During Peak Hours

BTC/USDT and ETH/USDT on major exchanges have some of the deepest order books in crypto - slippage on standard-sized trades is typically negligible. Before executing a larger order on any pair, check the bid-ask spread width: a narrow spread signals adequate depth, while a wide spread is a warning that your order will move the market. Peak liquidity hours (US-EU session overlap, roughly 13:00-17:00 UTC) generally offer tighter spreads across the board. Low-cap altcoin pairs amplify slippage risk at any hour.

Break Large Orders Into Smaller Chunks (TWAP / VWAP)

For trades large enough to visibly move the order book, splitting execution across time directly counters the "walking the book" problem described in the causes section.

📊 TWAP vs. VWAP - Quick Reference

TWAP (Time-Weighted Average Price): Executes equal-sized portions at fixed time intervals - e.g., buy $50,000 worth of ETH in 10 lots of $5,000 over 10 minutes.

VWAP (Volume-Weighted Average Price): Executes portions proportional to current market volume, benchmarking your average fill against the session average.

Advanced order types on exchanges like Kraken Pro and Binance support automated TWAP execution. Algorithmic trading tools and DeFi aggregators increasingly offer it too. For retail-scale trades below $10,000, manual splitting is usually sufficient. Understanding how funding rates and market structure affect your perpetual positions also helps contextualize why execution cost management - including slippage - compounds over time; you can explore that further in this guide to analyzing funding rates in crypto.

Slippage vs. Bid-Ask Spread vs. Price Impact

These three concepts are often conflated, and they're not the same thing - though they can all hit you in the same trade.

You can face all three simultaneously. A large market order on a volatile, illiquid pair during peak congestion will incur slippage (price moved between order and fill), a wide spread (poor entry price before you even start), and price impact (your own order moves the market against you).

Conclusion

Slippage in crypto is unavoidable at some level - but it's entirely manageable with the right execution habits. The gap between expected and actual fill price is driven by volatility, thin liquidity, large order sizes, and blockchain network delays. It behaves differently on CEXs and DEXs, and the consequences of ignoring it compound significantly over time.

Here's how to approach it by experience level:

- Beginners: Switch from market orders to limit orders on CEXs. This single change eliminates most slippage on standard trades. Stick to BTC/USDT and ETH/USDT until you understand order book mechanics.

- Intermediate traders: Master DEX slippage tolerance settings. Use the percentage thresholds by trade type above, and never leave tolerance on default for mid-cap or new token swaps. Understand MEV and how sandwich attacks target high-tolerance transactions.

- Advanced / high-volume traders: Incorporate TWAP or VWAP execution for positions large enough to impact the order book. Monitor bid-ask spreads and order book depth before entering, not after. Understanding liquidation dynamics is equally important - the liquidation heatmap guide covers how forced order cascades interact with price and liquidity.

Crypto markets are maturing rapidly - DEX liquidity is deepening, MEV protection tools are improving, and execution infrastructure is getting more sophisticated. Regardless of how the infrastructure evolves, understanding slippage mechanics remains a foundational trading skill. Platforms built on self-custody and on-chain verifiability - where every execution is transparent and auditable - reflect exactly the direction this market is headed. The traders who manage execution costs rigorously are the ones whose returns survive long enough to compound.

Crypto trading involves substantial risk of loss and is not suitable for all participants. This article is educational and does not constitute financial or investment advice. Last updated: March 2026.

Frequently Asked Questions

What is slippage in crypto in simple terms?

Slippage in crypto is the difference between the price you expected to pay (or receive) for a trade and the price you actually got when the trade executed. If you place a buy order for ETH at $2,000 but it fills at $2,020, your slippage is $20, or 1%. It happens because crypto prices move continuously, and there's always a delay between when you submit an order and when it executes. Market orders are most vulnerable - limit orders are the primary tool to prevent it on centralized exchanges.

What are the main causes of slippage in crypto trading?

There are four primary triggers. Market volatility moves prices between order submission and execution. Low market liquidity means your order has to fill across multiple price levels. Large order sizes exhaust the best available prices and push execution into worse levels. Finally, blockchain network congestion - unique to crypto - can delay DEX transactions for seconds to minutes while the market keeps moving. These causes often compound: a large order during high volatility on a low-liquidity altcoin is a worst-case scenario.

Is slippage always negative in crypto?

No - slippage is directional, not inherently negative. Positive slippage occurs when your buy order fills below the expected price, or your sell order fills above it, giving you a better outcome than planned. Negative slippage is the reverse and is far more common. Worth noting: some centralized exchanges retain positive slippage as part of their fee structure rather than passing the improvement back to you. Check your platform's execution policy to know which side of positive slippage you're on.

What is a good slippage tolerance for Uniswap in 2026?

The appropriate setting varies by trade type. For stablecoin swaps, 0.1-0.5% is generally sufficient. Major pair swaps (ETH, WBTC) work well at 0.5-1%. For mid-cap or newer tokens, 1-3% is typically necessary to ensure execution. Avoid setting tolerance above 5% - at that level, MEV bots can profitably sandwich your transaction. The "Custom" tolerance field in the Uniswap interface is where you input these values directly.

How do I calculate slippage percentage in crypto?

Use the formula: Slippage (%) = ((Executed Price - Expected Price) / Expected Price) . 100. If you expected to buy ETH at $2,000 and it filled at $2,040, your slippage is ((2,040 - 2,000) / 2,000) . 100 = 2%. A positive result means you overpaid on a buy order. On DEXs, this percentage is precisely what you're pre-authorizing when you set your slippage tolerance - the protocol reverts the transaction if actual slippage exceeds your threshold.

What is the difference between slippage and price impact in crypto?

Price impact is the effect your specific trade has on the market price - the larger your order relative to available liquidity, the more you move the price against yourself. Slippage is the realized gap between your expected and actual fill price, which price impact contributes to but doesn't fully explain. A trade can experience slippage from volatility alone with no meaningful price impact, or from significant price impact with minimal external volatility. On DEX interfaces, price impact is usually displayed separately from slippage tolerance.

What happens if my slippage tolerance is set too low on a DEX?

Your transaction reverts - it never executes. The DEX protocol compares your tolerance against the actual price impact at execution time. If the market has moved more than your allowed percentage since you submitted the transaction, the smart contract rejects the swap and returns your funds to your wallet (minus the gas fee already paid). The practical consequence is wasted gas and a missed trade. If your transactions frequently revert, raise your tolerance incrementally by 0.25-0.5% until you reach consistent execution, or wait for lower-congestion periods.