You've seen APY and APR on every staking platform and DeFi protocol you've visited - but do you actually know which one puts more money in your pocket? The difference between annual percentage yield and annual percentage rate isn't just semantics: it can meaningfully change the real returns on your crypto.

⚡ Quick Answer

APR (Annual Percentage Rate) is simple interest - it shows your return or borrowing cost for the year without factoring in compounding. APY (Annual Percentage Yield) includes the effect of compound interest, so it's always higher than APR when compounding occurs more than once a year. In crypto, APY is the more realistic metric for staking and yield farming, while APR is standard for lending and borrowing.

What Is APR in Crypto? 📊

APR, or Annual Percentage Rate, is the simplest interest measurement. It represents the annual return on an investment - or the annual cost of borrowing - calculated using straightforward simple interest, with no compounding involved.

In crypto, APR is most commonly used for lending protocols and borrowing platforms. When you supply assets to a DeFi protocol like Compound or Aave, the advertised rate is typically expressed as APR. It's also the standard for crypto-backed loans, where a lender quotes you a flat yearly interest rate.

How APR works in practice: If you stake 1,000 USDC into a lending pool at 8% APR, you'll earn exactly 80 USDC at the end of one year - regardless of when or how often the protocol distributes rewards. The calculation is linear and predictable: Principal . Rate . Time.

The simplicity of APR makes it useful for comparing borrowing costs. When you take out a crypto loan, you want the lowest APR possible - it tells you exactly what you'll owe.

What Is APY in Crypto? 📈

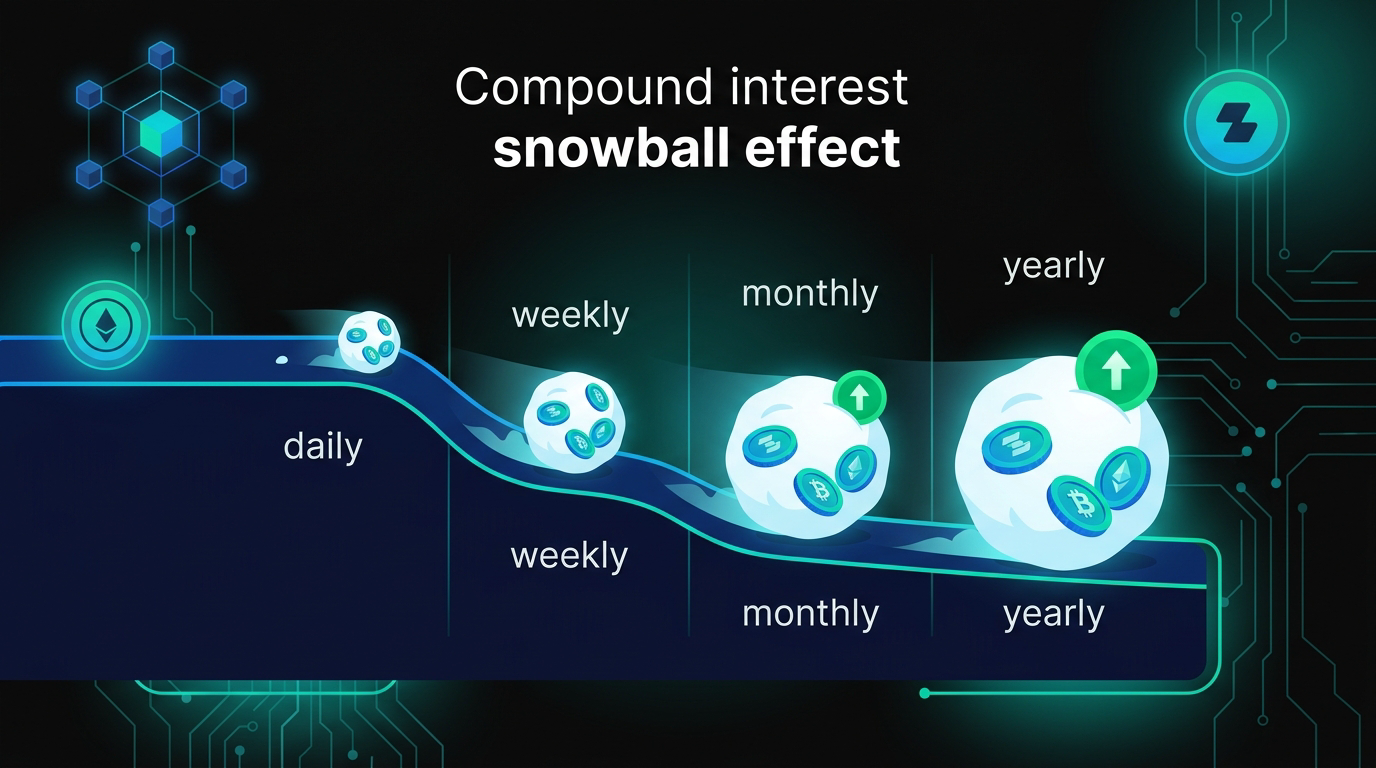

APY, or Annual Percentage Yield, is a more complete picture of your actual returns. It takes into account compound interest - meaning you earn returns not just on your original principal, but also on the returns you've already accumulated.

This is why staking platforms and yield farming protocols like Yearn Finance tend to advertise APY rather than APR. When rewards auto-compound - daily, hourly, or even per block in some protocols - the APY can be meaningfully higher than the headline APR, especially over long periods.

How APY works in practice: With a 10% APY and daily compounding, your 1,000 USDC grows to approximately 1,105 USDC by year end. That's 25 USDC more than the same 10% APR would generate - with no additional action on your part. The difference scales with the rate and the compounding frequency.

The formula for APY is: APY = (1 + r/n)^n - 1, where r is the stated annual rate and n is the number of compounding periods per year. For daily compounding (n=365) at 10%, this gives approximately 10.52% APY.

APY vs APR: Side-by-Side Comparison 🔍

Understanding both metrics together helps you make better decisions when choosing where to put your crypto. Here's how they stack up across the dimensions that matter most to investors in 2026.

The key rule of thumb: when you're earning, you want a higher APY. When you're borrowing, you want a lower APR. The two metrics serve opposite purposes - and conflating them is one of the most common mistakes crypto newcomers make.

A platform advertising 10% APR and a platform advertising 9% APY with daily compounding may offer almost identical actual returns. Always convert to a common metric before comparing.

🎯 Key Takeaways

- APR = simple interest - what you earn or owe without compounding

- APY = compound interest - the real yield after reinvestment kicks in

- APY is always equal to or greater than APR for the same base rate

- The more frequently compounding occurs, the wider the gap between APY and APR

- When earning: maximize APY. When borrowing: minimize APR.

APY vs APR in DeFi Staking and Lending 🏦

In practice, how APY and APR are used in crypto depends on the type of product you're interacting with.

Staking: Most proof-of-stake networks and delegated staking products advertise APY because rewards auto-compound. When you stake ETH on a platform like Lido or delegate SOL to a validator, your earned rewards are periodically added back to your staked balance - and future rewards are then calculated on the larger total. According to Binance Academy, this compounding distinction can significantly change returns over time.

Yield Farming and DeFi Protocols: Platforms like Yearn Finance automate the compounding process entirely. Rather than manually reinvesting rewards, Yearn's vaults reinvest yields continuously across multiple protocols - and the resulting APY can compound much faster than traditional finance. This is why protocols like Compound or Aave may show different APR numbers on the borrow and supply sides of the same asset.

Lending and Borrowing: When you supply assets to a lending protocol, you typically see APY (because your deposited balance compounds as interest accrues). When you borrow, you see APR - because the lender wants you to see a clean, simple cost figure without the compounding confusion. This deliberate asymmetry can make borrowing look cheaper than it is. Always check whether the loan charges compound interest on your outstanding balance.

Token Inflation Risk: One critical nuance: some DeFi protocols advertise very high APYs by minting new tokens as rewards. A 200% APY paid in a new governance token sounds impressive - but if that token loses value faster than rewards accumulate, your real return in dollar terms may be negative. This is why compound interest crypto metrics need to be evaluated alongside the underlying token's price stability.

⚠ Risk Warning

Very high APYs in DeFi - anything above 50-100% - are almost always accompanied by elevated risk: token inflation, smart contract vulnerabilities, impermanent loss in liquidity pools, or lock-up periods. A 300% APY in a new governance token is not the same as a 5% APY on a battle-tested stablecoin pool. Always evaluate the source of the yield before committing capital.

Your signal won't wait for KYC

Connect wallet, open a perp in 30 seconds on ZEXO. No email, no ID, no account.

Trade on ZEXO →How to Calculate APY from APR 🧮

Knowing the formula lets you compare any two crypto products on equal terms, regardless of how each platform chooses to display its rates.

The APY formula:

APY = (1 + r/n)^n - 1

Where: r = annual interest rate (as a decimal), n = number of compounding periods per year

Practical examples using this formula:

| Scenario | APR | Compounding | Resulting APY |

|---|---|---|---|

| ETH staking (monthly rewards) | 4.0% | 12. per year | ~4.07% |

| USDC lending pool (daily compound) | 8.0% | 365. per year | ~8.33% |

| High-yield DeFi vault (hourly) | 20.0% | 8,760. per year | ~22.13% |

| Savings account comparison | 5.0% | 12. per year | ~5.12% |

The gap between APR and APY is small at lower rates but widens significantly at higher rates - which is why the metric choice matters most in high-yield DeFi strategies, not traditional savings.

Converting APY back to APR (useful when comparing across platforms):

APR = n . [(1 + APY)^(1/n) - 1]

Most DeFi dashboards show APY because it looks more attractive for marketing purposes. Understanding how to reverse-engineer the underlying APR helps you identify when a platform is packaging the same base rate differently from a competitor.

Explore how Yearn Finance automates this optimization across multiple protocols simultaneously, compounding at rates that would be impractical to manage manually.

Frequently Asked Questions

Is APY always better than APR?

APY is a more complete metric for measuring earning potential because it accounts for compounding. However, "better" depends on context: when borrowing, you want a low APR; when earning, you want a high APY. A high APY on a volatile or inflationary token may still result in poor real returns. Always evaluate both the rate and the quality of the underlying yield source.

Why is APY higher than APR?

APY includes the effect of compound interest, which means you earn returns on returns already accumulated. The more frequently compounding occurs - daily vs monthly vs yearly - the larger the gap between APY and the underlying APR. At a 10% base rate with daily compounding, APY reaches approximately 10.52%.

How does APY vs APR affect crypto staking returns?

In staking, rewards are typically expressed as APY because many protocols auto-compound. If rewards are distributed and automatically re-staked, your effective annual yield (APY) will be higher than the simple rate (APR). ETH staking, for example, typically quotes 3-5% APR, but with auto-compounding validators the effective APY can be slightly higher depending on reinvestment frequency.

What is a good APY for crypto in 2026?

This depends on the risk level. For stablecoin yield farming or lending, 4-12% APY is considered reasonable. ETH or BTC staking typically offers 3-6% APY. Anything above 50% APY generally carries elevated risk from token inflation, protocol risk, or impermanent loss. Higher rates in DeFi platforms are possible but require careful due diligence.

Can APR and APY be the same?

Yes - if compounding occurs only once per year, APR and APY are mathematically equal. In practice, most crypto protocols compound more frequently than annually, so there's almost always a gap between the two figures.

How do I know if a crypto platform is showing APR or APY?

Always read the fine print on any staking, lending, or yield farming platform. Look for disclosures like "compounded daily" or "simple interest rate" near the quoted percentage. If neither is specified, ask the platform directly or check their documentation before committing funds.

Conclusion

The difference between APY vs APR in crypto is straightforward once you know the rule: APR is simple interest, APY includes compounding. But in practice, that distinction can have a real impact on your returns - especially in DeFi, where compounding may happen hourly or per block.

The rule to remember: maximize APY when earning, minimize APR when borrowing. Always convert rates to the same basis before comparing two platforms. And when you see a triple-digit APY, ask what's actually generating that yield - because compound math can't rescue a depreciating token.

For a deeper look at how to put your crypto to work through staking and yield optimization, explore ZipUp - Zipmex's flexible earning product for BTC, ETH, and USDT.

Stop depositing. Start trading.

ZEXO perps execute straight from your wallet. No deposits, no withdrawals, no waiting.

Open ZEXO →⚠ Disclaimer: The information provided in this article is not intended to provide investment or financial advice. Investment decisions should be based on the individual's financial needs, objectives, and risk profile. We encourage readers to understand the assets and risks before making any investment entirely. Cryptocurrency investments are subject to high market risk. Past performance does not guarantee future results.